Portfolio Management

Portfolio in Motion: How Agility, Intelligence and ESG Are Rewriting Corporate Real Estate

Portfolio in Motion: How Agility, Intelligence and ESG Are Rewriting Corporate Real Estate

Real estate portfolios, once built on long-term leases and predictable headcounts, are being reshaped to prioritise agility, efficiency, and alignment with corporate purpose. This evolution is not just visible in market narratives: it’s grounded in data.

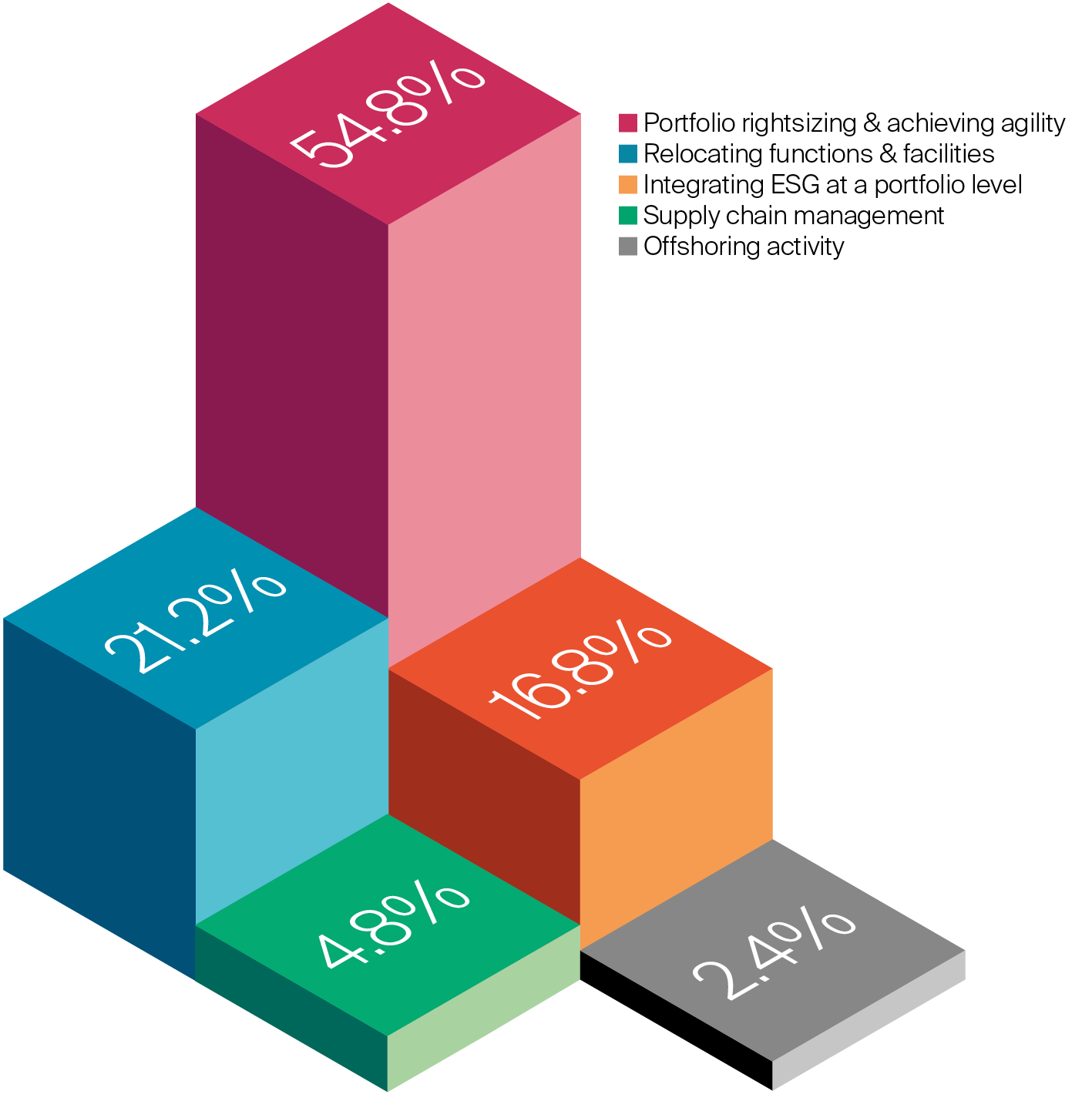

According to the latest survey, rightsizing and achieving agility emerged as the single most pressing portfolio level challenge for occupiers, with 55% of respondents selecting it in this second challenge area. This result reflects the industry-wide reckoning with hybrid work, underutilised assets, and rising cost pressures. That reckoning will translate into action over the next five years. Companies are trying to reshape their portfolios to better match current usage and future flexibility needs.

Trailing behind, though still significant, were concerns about relocating functions and facilities (21%), integrating ESG at a portfolio level (17%), supply chain management (5%), and offshoring activity (2%). While some of these responses may be smaller in number, they reflect high-impact shifts in how companies manage space in direct response to broader operational challenges. They are also more function specific rather than being universal in their nature. As such, they should not be under-estimated as challenges for some.

These findings offer a valuable lens through which to examine the five key forces influencing corporate real estate portfolio management today.

By % of respondents (n=292)

The dominance of rightsizing as a major challenge is no surprise. The shift to hybrid and remote work has made large, fixed office footprints inefficient. Corporate occupiers are asking hard questions: How much space do we really need? Where should it be located? What functions must be central, and what can be distributed?

Rightsizing today is about selectivity and intentionality. Organisations are consolidating into higher-quality, amenity-rich buildings that support collaboration, while divesting surplus space or converting it to more flexible formats. Companies like Salesforce and HSBC have significantly trimmed their footprints, investing instead in prime hubs and experience-led campuses. Data is central to this transformation. From badge swipe data to occupancy sensors, occupiers are using technology to quantify usage and reconfigure space accordingly.

By % of respondents (n=163)

Crucially, rightsizing doesn’t always mean shrinking. In fact, despite the prevalence of rightsizing as a challenge and focus for CRE professionals, half of all respondents to (Y)OUR SPACE anticipate their portfolios becoming larger over the next 3-5 years, compared to one-fifth who expect their total footprint to reduce.

So rightsizing is nuanced and not a one-track trend. In some cases, it can mean expanding into the right kind of space: better located, more agile or better aligned with business priorities. As organisations grow in new markets, shift towards more project-based work, or bring functions back in-house, the demand for space can evolve in unexpected ways.

Rightsizing is about matching supply with purpose. That could mean trading a large, underutilised HQ for a network of smaller, collaborative hubs, or reinvesting in flagship locations that reinforce culture and brand. The goal isn’t less space - it’s smarter, more appropriate space.

Yet beneath the strategic logic of rightsizing lies a more complex organisational reckoning. Many businesses are confronting cultural and political tensions as they reshape their portfolios. For some, legacy offices carry symbolic weight - seen as markers of status, stability or identity - making their downsizing a delicate internal conversation. In other cases, business units compete for square footage based on historical entitlements rather than current usage patterns, resisting centralised decision-making.

There are also disparities in how teams use space: legal or finance may visit the office sparingly, while product or client-facing roles rely on physical presence. As well as being chronically absent from the narrative of recent years, these variations complicate blanket portfolio strategies. The result is growing emphasis on change management, stakeholder alignment, and scenario planning - not just architectural or locational decisions. Rightsizing, done well, demands not only data but diplomacy.

A key priority for many organisations today is ensuring that the right work happens in the right places. This means critically evaluating whether corporate functions, support services, and operational roles are best delivered from central offices, regional hubs, or entirely new locations. The shift isn’t just about cost. It’s about operational resilience, performance, agility, and talent alignment.

Companies are increasingly relocating functions based on a matrix of factors: access to specialised skills, operational cost, and business resilience. Shared service centres, R&D labs, call centres, and logistics operations are all being re-evaluated considering these dynamics too. Real estate strategy is no longer confined to the traditional office. It’s about orchestrating a network of physical assets that supports a business’s broader goals - be that global reach, innovation, or customer proximity.

This relocation of functions is also prompting a more nuanced approach to location strategy. Proximity to customers, access to future talent, and regional incentives are now central considerations in deciding where work is best placed. Tech firms, for instance, are setting up engineering hubs in emerging talent markets, while pharmaceutical companies cluster research teams near academic and clinical ecosystems. The era of a single, all-purpose headquarters is giving way to a more distributed, purpose-led footprint.

Hybrid models are reinforcing this shift, allowing organisations to move fluidly between centralised and decentralised delivery. In some cases, this means a blend of flagship HQs and regional anchors. In others, it includes a network of smaller satellite offices, co-working partnerships, and remote-first infrastructure. As businesses recalibrate their operating models, real estate must keep pace: offering flexibility without fragmentation.

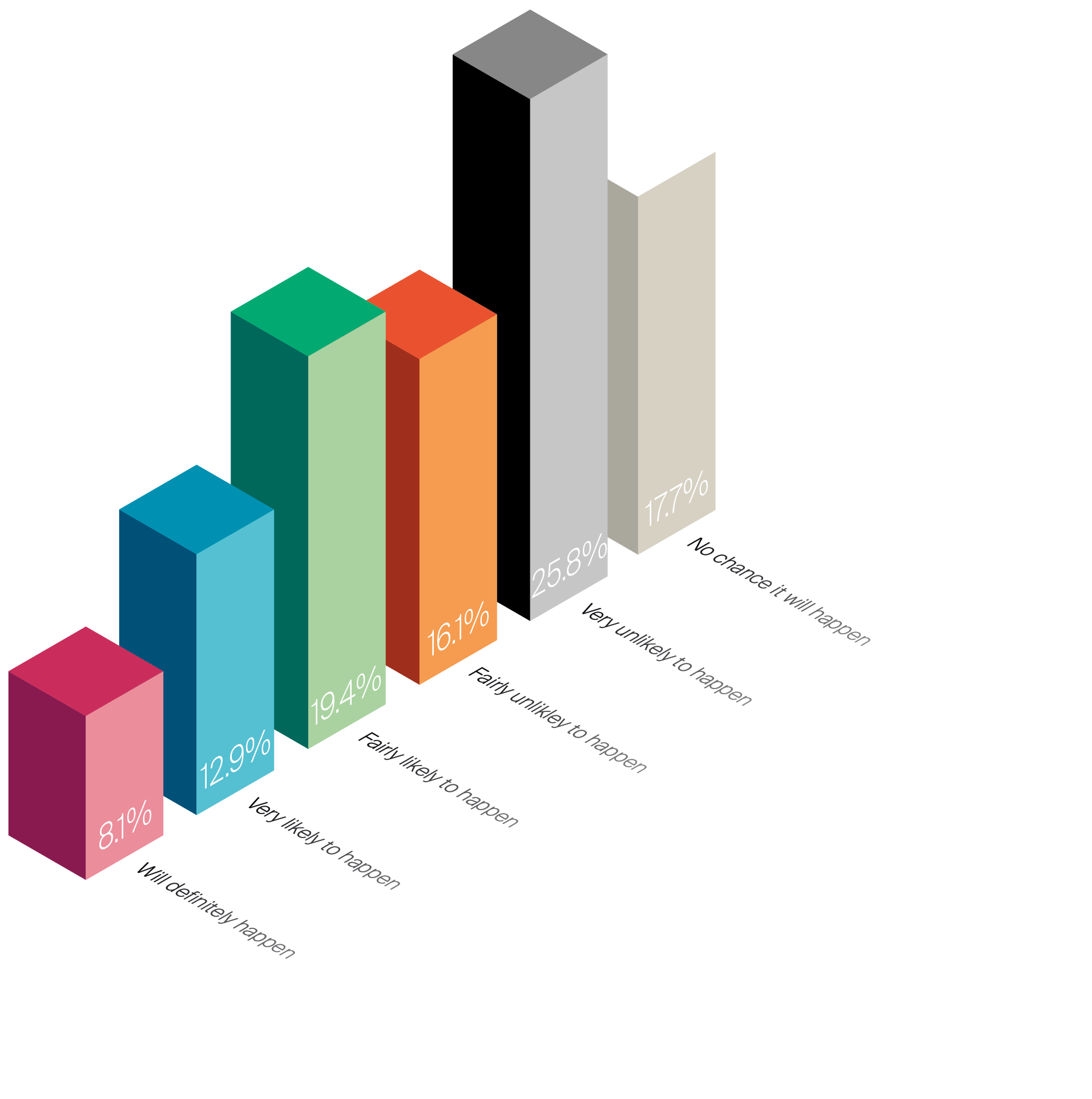

Thirty-nine per cent of those respondents identifying relocation as their biggest challenge in portfolio management, thought it likely that their core HQ facilities would be relocated within the next 3 years – broadly in-line with the response to the same question in the third edition of (Y)OUR SPACE published in 2023.

By % of respondents (n=62)

Importantly, these shifts also elevate previously overlooked parts of the portfolio. Spaces like training centres, customer labs, and logistics facilities are being repositioned as strategic assets, not operational afterthoughts. They are becoming sites of innovation, brand-building, and employee engagement. As organisations seek to align their footprint with functional intent, workplace design and investment are following suit supporting not just where people work, but how work gets done.

In this new geography of work, success lies in the ability to continuously adapt the portfolio to reflect changing business needs. That means corporate real estate strategies must be agile, data-informed, and closely aligned with where and how value is created across the organisation. It is no longer about maintaining a static set of locations. It’s about curating a portfolio that actively supports growth, resilience, and transformation.

Forty-nine respondents (17%) to the latest (Y)OUR SPACE survey cited ESG integration as their biggest challenge. While this may trail rightsizing in urgency, the long-term implications are profound. With regulators, investors, and talent all demanding climate accountability, CRE is fast becoming a decarbonisation battleground.

Occupiers are prioritising green-certified buildings, low-carbon construction materials, and smart energy systems. Companies such as Amazon, Google, and L’Oréal are designing net-zero roadmaps for their global portfolios.

Yet, the trend goes beyond environmental targets. Social and governance considerations are also influencing CRE decisions: from inclusive workplace design to the ethical procurement of services. Increasingly, occupiers view ESG as a value driver, not just a compliance exercise.

Although fewer respondents (14 or 5%) identified supply chain management as their top concern, its importance is growing - particularly as global disruptions make operational continuity a boardroom issue.

Real estate portfolios are being reconfigured to support more resilient, regionalised supply chains. This includes investment in distribution hubs, proximity to ports or multimodal transit networks, and the integration of warehouse/logistics infrastructure with office and support functions.

In sectors like manufacturing, retail, and life sciences, CRE strategy is now directly supporting supply chain transformation, ensuring product flow, supplier agility, and customer delivery are not compromised by external shocks.

Expect to see more collaboration (if not integration) between CRE leaders and supply chain teams in deciding on location, footprint size, and design for industrial and mixed-use facilities.

While only a small percentage (2%) of respondents flagged offshoring as their primary challenge, its strategic implications remain significant. Offshoring is no longer a one-size-fits-all solution driven by labour arbitrage alone. Instead, companies are reevaluating which roles, regions, and risks are best served by offshore models.

Some are reshoring or nearshoring to improve control, mitigate geopolitical risks, or align with talent and ESG considerations. Others continue to use offshore locations but in more targeted, digitally enabled ways.

For CRE professionals, this shift requires dynamic portfolio planning that accommodates fluctuation in international footprint size, cultural expectations, and operational dependencies. The office, service centre, or tech hub in Bangalore, Manila or Kraków must be managed with the same agility and precision as the HQ.

The (Y)OUR SPACE survey underscores what the market is already sensing: portfolio management is no longer just an operational discipline; it is a strategic act. Rightsizing, ESG integration, location planning, cost control, and tech enablement are deeply interwoven. They require cross-functional collaboration, high-quality data, and a willingness to rethink old norms.

As organisations navigate the next cycle of economic and workplace transformation, the most successful ones will treat their real estate portfolio as a living, evolving ecosystem not a fixed asset base. In that sense, the future of portfolio management is not about buildings; it’s about adaptability, intelligence, and purpose.

Get the latest occupier trends and insights in your inbox.

(Y)our Space

Welcome to the fourth edition of (Y)OUR SPACE—Knight Frank’s global research campaign that explores the forces reshaping work, workplace, and the real estate strategies evolving in response.

01 December 2025

(Y)our Space

Findings from the latest (Y)OUR SPACE survey suggest that corporate real estate (CRE) is entering a defining phase—one shaped not by a single disruptor, but by a complex interplay of strategic, economic, and operational catalysts.

01 December 2025

(Y)our Space

The challenges facing corporate real estate.

01 December 2025

(Y)our Space

At the Sharp End: What CRE Leaders Are Telling Us About Supporting Growth and Transformation

01 December 2025

(Y)our Space

Portfolio in Motion: How Agility, Intelligence and ESG Are Rewriting Corporate Real Estate

01 December 2025

(Y)our Space

Pressure Points: The Top Challenges Shaping Workplace Strategy

01 December 2025

(Y)our Space

6 Hard Truths for CRE teams and the Smart Moves key to their future relevance and impact.

01 December 2025

Sorry!

An unexpected error has occurred.

Please try again later.