Insight 1: Easy Said, Easy Done?

6 Hard Truths for CRE teams and the Smart Moves key to their future relevance and impact.

6 Hard Truths for CRE teams and the Smart Moves key to their future relevance and impact.

The setting felt fitting: a resilient, inventive, globally connected city remade repeatedly across centuries.

The theme of the panel session I convened and chaired – entitled Hard Truths, Smart Moves – was about precisely that spirit. After introducing some of the key arguments from the fourth edition of (Y)OUR SPACE to underscore the scale of the challenge facing CRE leaders and the battlegrounds ahead, I was joined by Shelley Frost, Global Head of Real Estate Strategy at DSM-Firmenich; Toby Chapman, Global Workplace Strategy Director at Arcadis; and Philip Cohen, Category Manager for Real Estate Facilities in Europe at Securitas Group. With a century of combined experience and expertise, our panellists offered tips on navigating volatility, acting purposefully, and moving decisively from ideas to execution.

This powerful and (thankfully!) popular session identified six hard truths facing CRE, and suggested six smart moves that CRE leaders must make to retain relevance, influence, and impact.

There is a paradox at the heart of corporate real estate. For decades, the industry has asserted that real estate is far more than a box to put people in. The workplace has been recognised as a level for culture, a catalyst for collaboration, a magnet for talent, and a statement of brand. Portfolio choices have been shown to support broader strategic ambitions – whether entering new markets, meeting sustainability goals, or reshaping cost structures – and, done well, they can confer genuine competitive advantage.

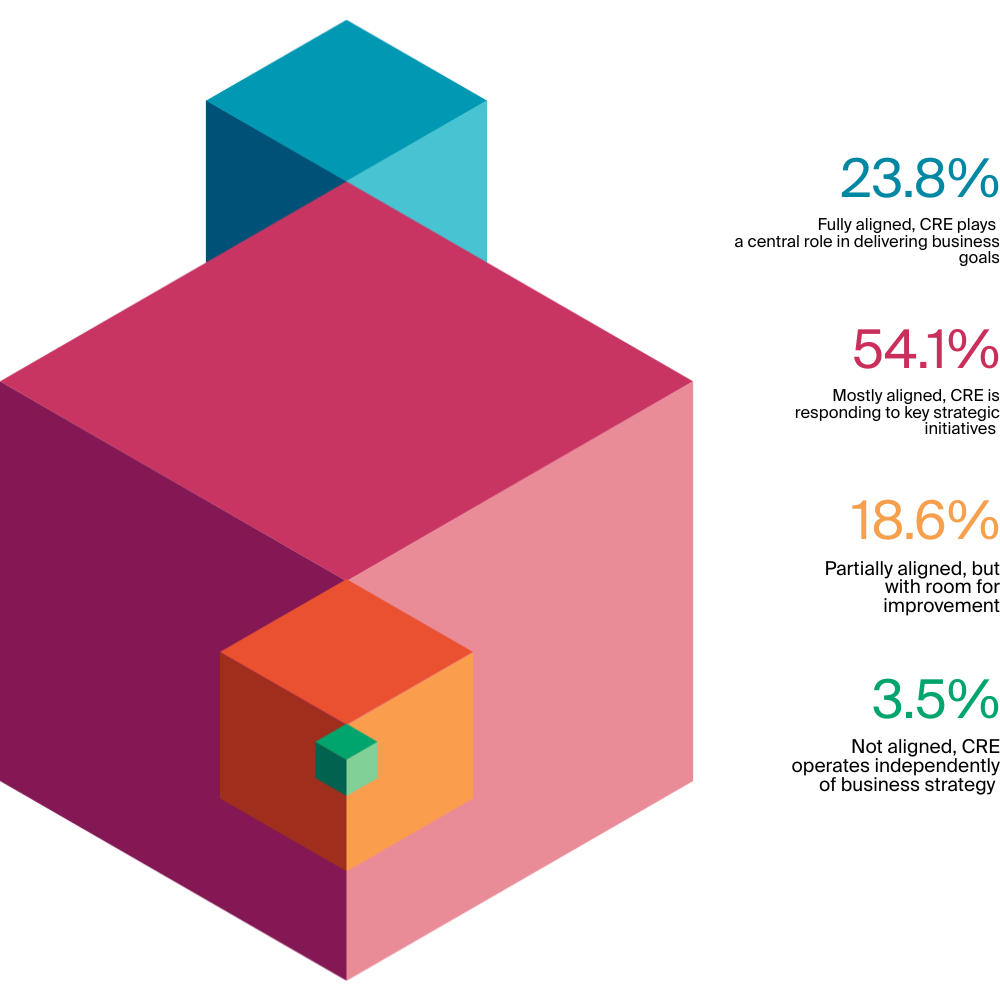

Yet despite this recognition, the hard truth is that the CRE function still sits downstream from strategy formulation. The latest edition of (Y)OUR SPACE makes this painfully clear: only 23.8% of leaders maintain that their CRE strategy is fully aligned; real estate plays a central role in delivering business goals. A majority (54.1%) say they are mostly aligned but crucially act in a responsive capacity. Another 18.6% admit only partial engagement, with the remaining 3.5% observing no alignment. In essence, three-quarters of surveyed real estate leaders operate downstream from strategy and serve as interpreters of strategy, not co-authors.

The smart move is for CRE leaders to break the paradox – not necessarily by continuing to call for a seat at the boardroom table (which seems for most unreachable) – but to recast themselves as strategic business partners. They must get closer to the place and time where growth and transformation plans, cultural shifts, and commitments are conceived.

According to our panellists, that means bringing hard facts and evidence to the business, in a language that they (as non-real estate specialists) can understand. The role is increasingly to factually illustrate how portfolio strategies enable market entry speed, resilience against geopolitical disruption, underscore talent strategies, or are central to the effective delivery of net-zero pathways.

In short, the paradox can only be resolved when real estate functions move upstream into shaping ambition – not downstream in executing it.

By % of respondents (n=113)

Periods of turbulence were once viewed as temporary interruptions to business as usual. But in 2025, volatility is business as usual. Tariff shocks, disrupted supply chains, shifting trading blocs, inflation, and rapid technological change now collide with such frequency that disruption has become the defining operating environment. In this climate, corporate real estate cannot sit back and wait for calmer waters – because waves of disruption are here to stay. Waiting for clarity before acting can mean being overtaken by competitors willing to make ambiguous decisions.

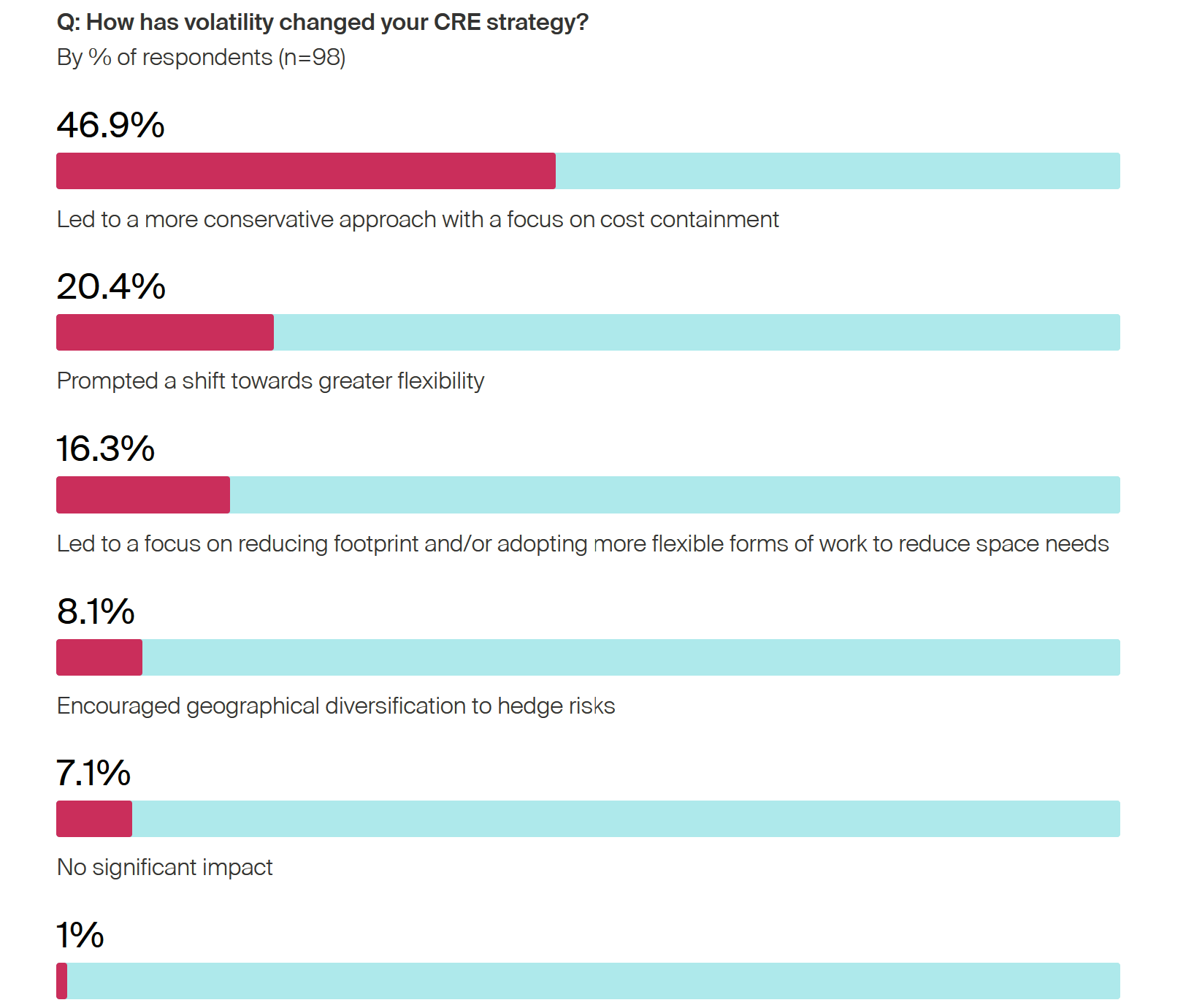

The hard truth is that volatility should be the spark for transformation, yet too often it drives organisations into retreat. Transformation requires bravery – investment in new markets, adoption of new models, and a willingness to take risks. However, the instinctive response to volatility at the enterprise level and within CRE is to play conservatively. This has been the playbook of the post-pandemic period. (Y)OUR SPACE data illustrates the point – almost half of all respondents say volatility has led them to adopt a more conservative approach focused on cost containment.

Only a minority report using volatility to fuel greater flexibility (20.4%) or footprint reconfiguration (16.3%). Less than 10% have diversified geographically to hedge geopolitical/geoeconomic risk. And yet, at the same time, almost 70% of companies anticipate offensive transformation strategies in the next five years – from entering new markets (19.9%) to digital transformation (18.4%), business diversification (15.4%) to strategic acquisitions (14.8%). The contradiction is apparent: volatility demands bold change, but the reflex is often to pull back.

The smart move is to get on the front foot. The organisations that will thrive are those whose CRE leaders resist the pull of conservatism and lean into transformation. That means:

The message from Amsterdam was clear: volatility is not a reason to pause – it is the reason to accelerate.

By % of respondents (n=98)

The conversation around rightsizing is often clouded by negative associations – reductions, retreat, retrenchment. But the reality, as revealed in (Y)OUR SPACE, is far more nuanced. Rightsizing is not just about shrinking footprints; it is about optimising. It is about realigning portfolios with shifting business models, new patterns of work, and emerging financial realities. As I have been saying during the recent (Y)OUR SPACE tours in India, Singapore and Australia, rightsizing is a make-over, not a haircut.

The hard truth is that rightsizing is necessary but difficult – a wrong move can be operationally damaging and financially punitive. After the shock of the pandemic and the genie coming out of the bottle on flexible working, office occupancy signals are becoming clearer and more stable. At the same time, financial pressures are intensifying, whilst the deferrals of decisions in recent years have given way to the need for more definitive decision-making.

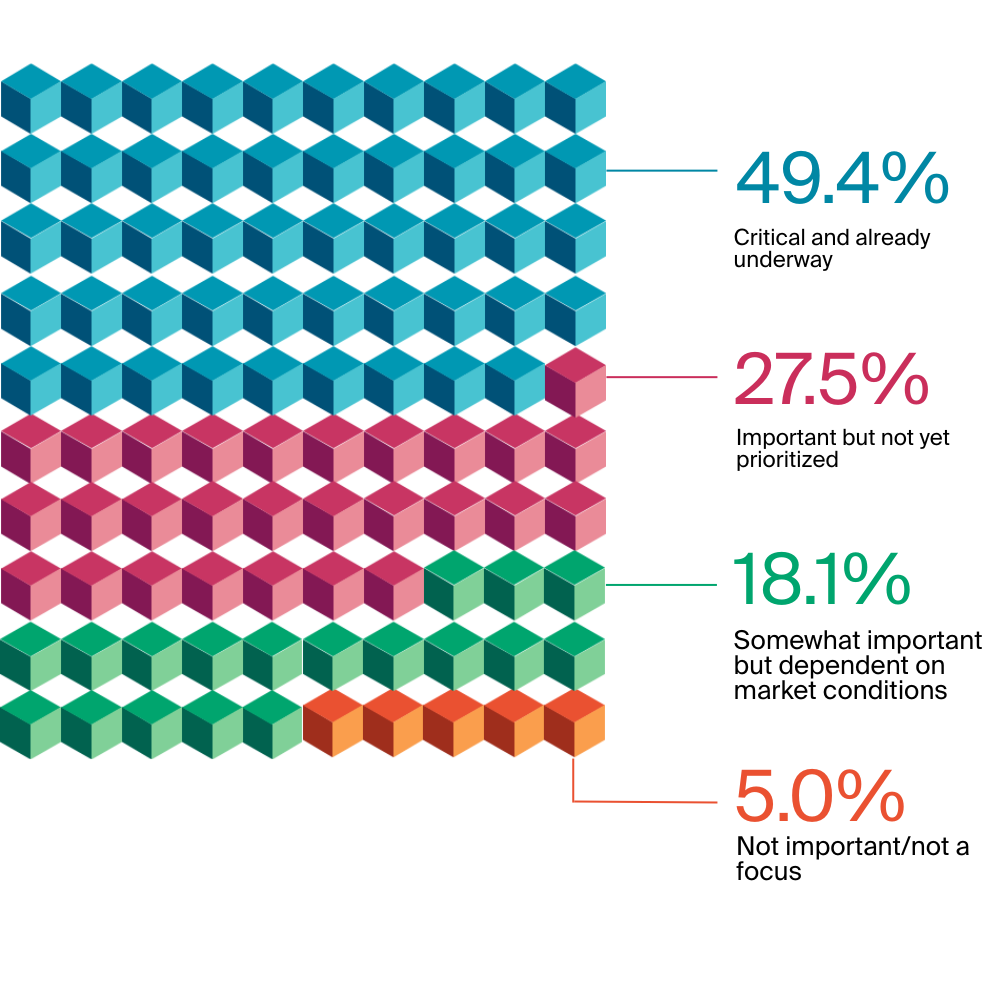

Accordingly, nearly half of occupiers surveyed in (Y)OUR SPACE saw rightsizing as critical and already underway, with a further quarter regarding rightsizing as important but not yet prioritised. In this sense, more than three-quarters of CRE leaders see rightsizing as necessary for aligning portfolios with business strategy.

The drivers go beyond simple cost reduction. Almost 40% of leaders surveyed cite cost pressures, but one third point to changes in business operations and footprint, while a further fifth highlight the increased adoption of hybrid workstyles. In other words, rightsizing is driven as much by strategic transformation as by financial strain.

The hard truth is that rightsizing in the real world is not a synonym for cuts. It is a recalibration, often complex, and increasingly essential to ensure CRE portfolios fully reflect how businesses actually operate.

By % of respondents (n=160)

For CRE leaders, the smart move in effectively navigating rightsizing is to frame it as alignment, not austerity. That requires:

One message emerged from our panel regarding rightsizing: It is not about doing less; it is about doing what matters most.

Relocation has always been one of the most consequential levers in corporate real estate. Unlike lease renegotiations or incremental adjustments to the footprint, a relocation is visible across the organisation and felt by every stakeholder. It disrupts routines, carries financial and operational risk, and exposes leadership to scrutiny. However, precisely because of its visibility and impact, relocation can also deliver extraordinary strategic benefits. It can reset a company’s relationship with talent, reposition it within innovation ecosystems, and align the business more closely with environmental or cultural ambitions.

The scale of relocation that lies ahead is hard to ignore. (Y)OUR SPACE shows that 40% of CRE leaders expect relocation activity in the coming cycle. These are not small-scale shifts: they include headquarters, core R&D hubs, and production or operations centres – the kinds of moves that can alter the trajectory of entire businesses. The 40% could be underestimated given the ongoing impacts of tariffs, trade wars and the potential emergence of more regionalised operational models to mitigate risk.

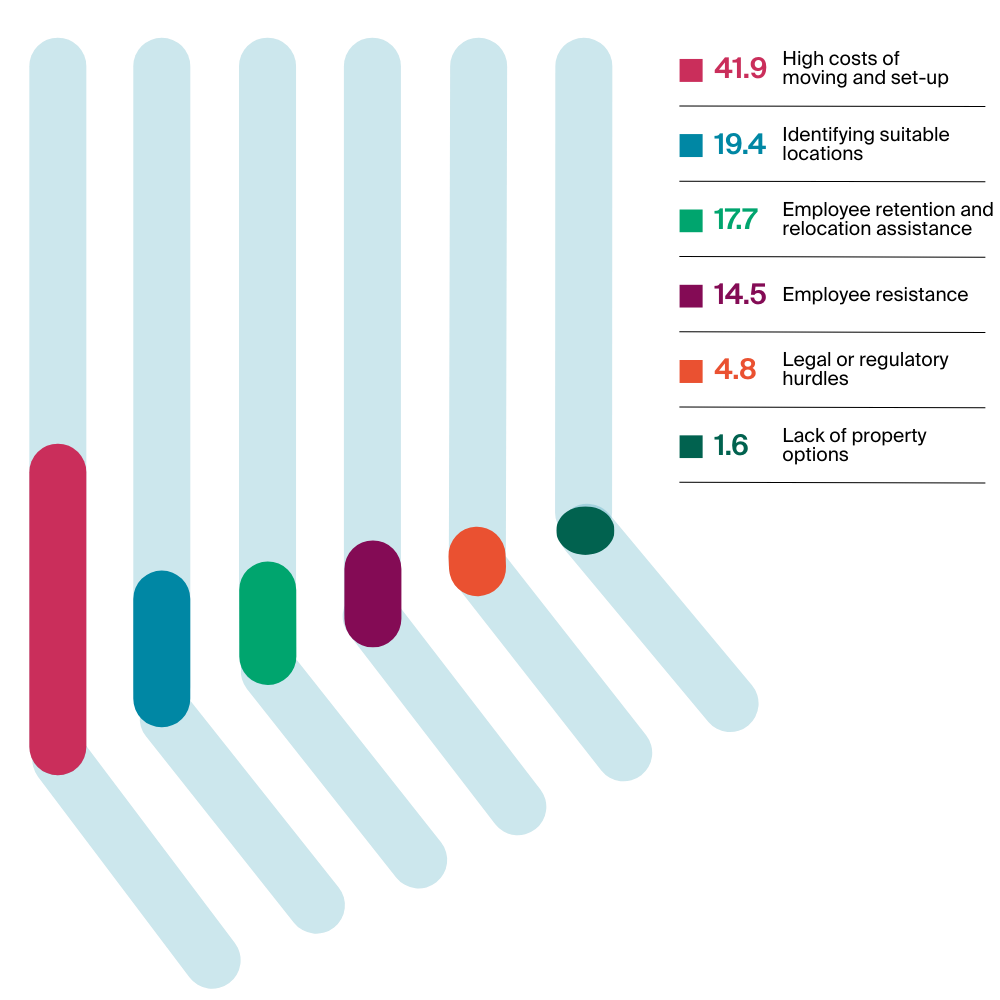

Yet the hard truth is that delivery remains fraught with obstacles, whatever the volume of future relocations. The high costs of moving and set-up dominate as the number one challenge, cited by 41.9% of CRE leaders. Close behind are the complexities of identifying suitable locations and managing employee retention and relocation assistance. Employee resistance adds another dimension, reminding us that the human response to relocation can make or break success. And while fewer respondents cite regulatory hurdles or a lack of options, these can still derail plans in specific markets.

The hard truth is this: relocation is both high-cost and high-risk. It cannot be undertaken lightly, and when the rationale is unclear or poorly communicated, the risks can often outweigh the rewards. Moves that are reactive to lease expiries or short-term incentives risk being remembered as costly disruptions rather than strategic accelerators.

By percentage of respondents (n=62)

So what is the smart move? The organisations that will turn relocation from risk into opportunity will put purpose at the centre of the decision. That means:

In an era of obsolescence, relocations are rising – but the dividing line will be between those driven by purpose and those that are reactive.

The debate over the office has often been reduced to a numbers game: how many days in, how many days out? However, focusing on presence misses the bigger question: performance. The workplace cannot simply be a neutral backdrop. It must actively enable culture, productivity, and collaboration. The office is competing for attention in a world of hybrid and increasingly varied workstyles. If it does not deliver value, employees will vote with their feet.

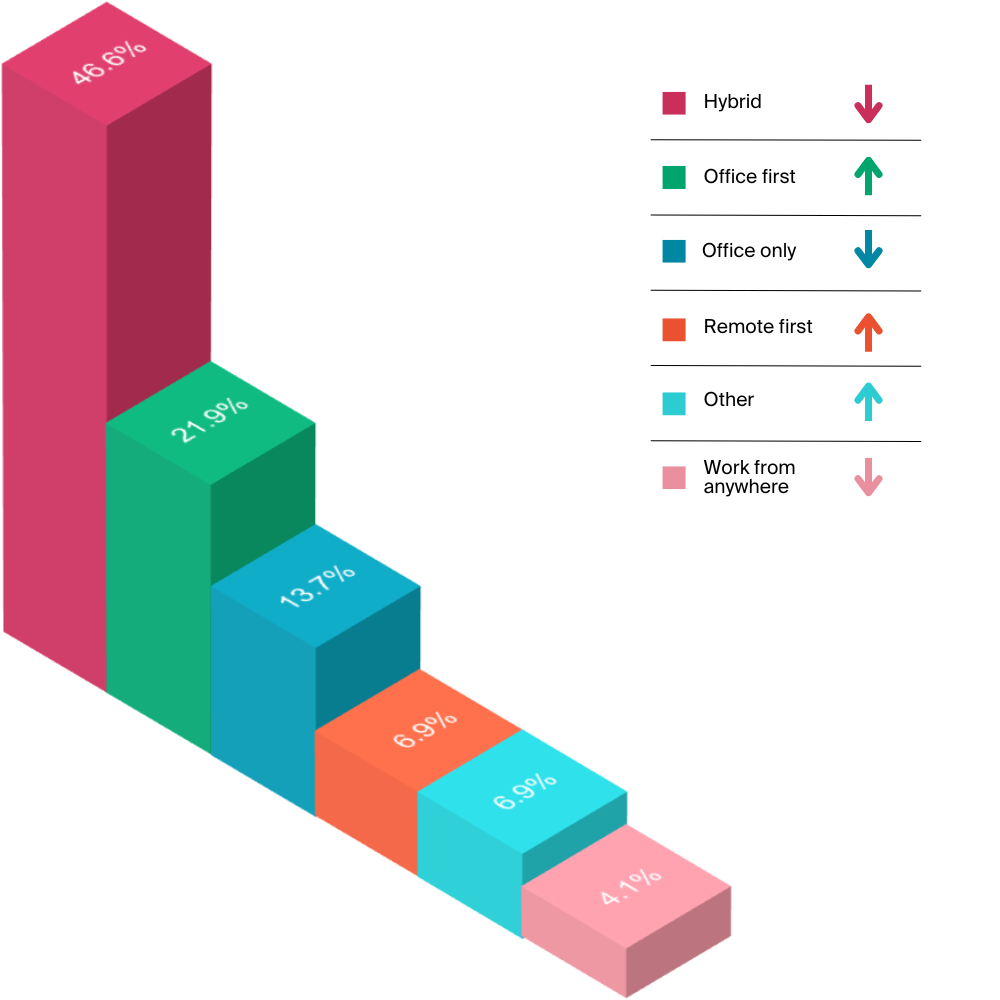

The hard truth is (for most) there is no return to the old 5 days a week, 7 hours a day in office workstyle. Workstyles are fragmenting, and this has a direct impact on the workplace. According to (Y)OUR SPACE 2025, nearly half of organisations (46.9%) expect to be hybrid in three years, but significant proportions anticipate “office-first” (21.9%) or even “office-only” (13.7%) approaches. A smaller share leans toward “remote-first” (8.9%) or “work-from-anywhere” (4.1%). The future of work continues to have the office as a fundamental setting, but our relationship with the office will be more fluid and flexible.

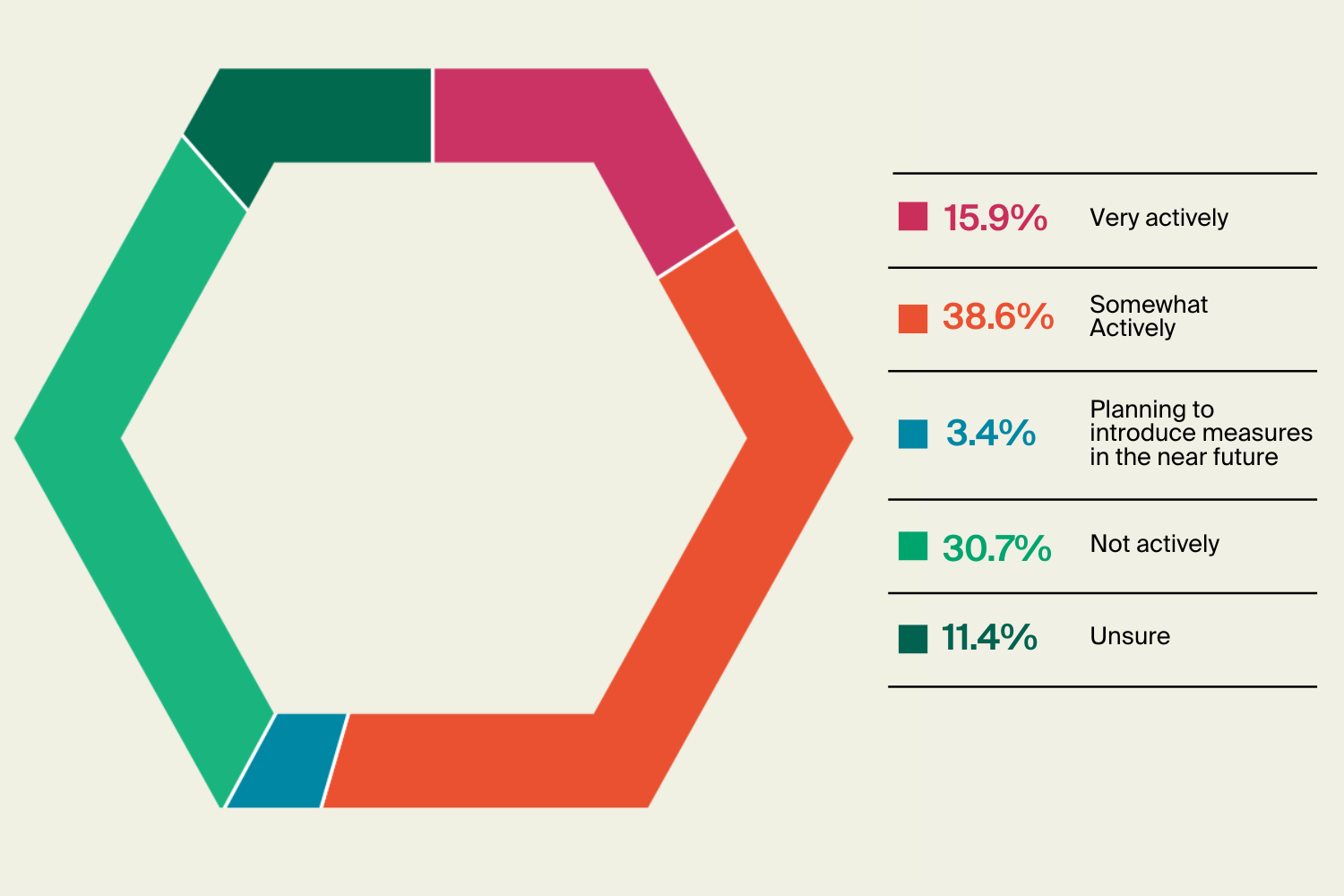

Because of this, one reality cuts across them all: occupancy is volatile. Employees do not spread attendance evenly across the week, leading to overcrowding peaks and underuse troughs. Our data shows that only 15.9% of organisations are actively taking steps to reduce this variance, while 38.6% are somewhat active and 30.7% admit to doing nothing. The result is wasted capacity at one end and strained experiences at the other.

The hard truth is that serious attempts to reduce the ‘delta’ between peak and trough occupancy (making the office more financially efficient) will inevitably require a trade-off: removing some employee flexibility. Coordinating anchor days and directing attendance means dictating employees’ days in the office. Efficiency gains will therefore come at the expense of individual choice.

By % of respondents (n=73)

Arrows show collective movement from current position

By % of respondents (n=88)

That tension cannot be wished away. Underperforming workplaces that do nothing will remain liabilities, wasting space and eroding confidence, collaboration and culture. However, workplaces that work must accept that performance may come with a cost to flexibility.

Smart moves by CRE leaders need to confront this trade-off head-on and manage it transparently:

In Amsterdam, one theme was consistent: employees will not return to offices that simply exist; they will return to workplaces that perform.

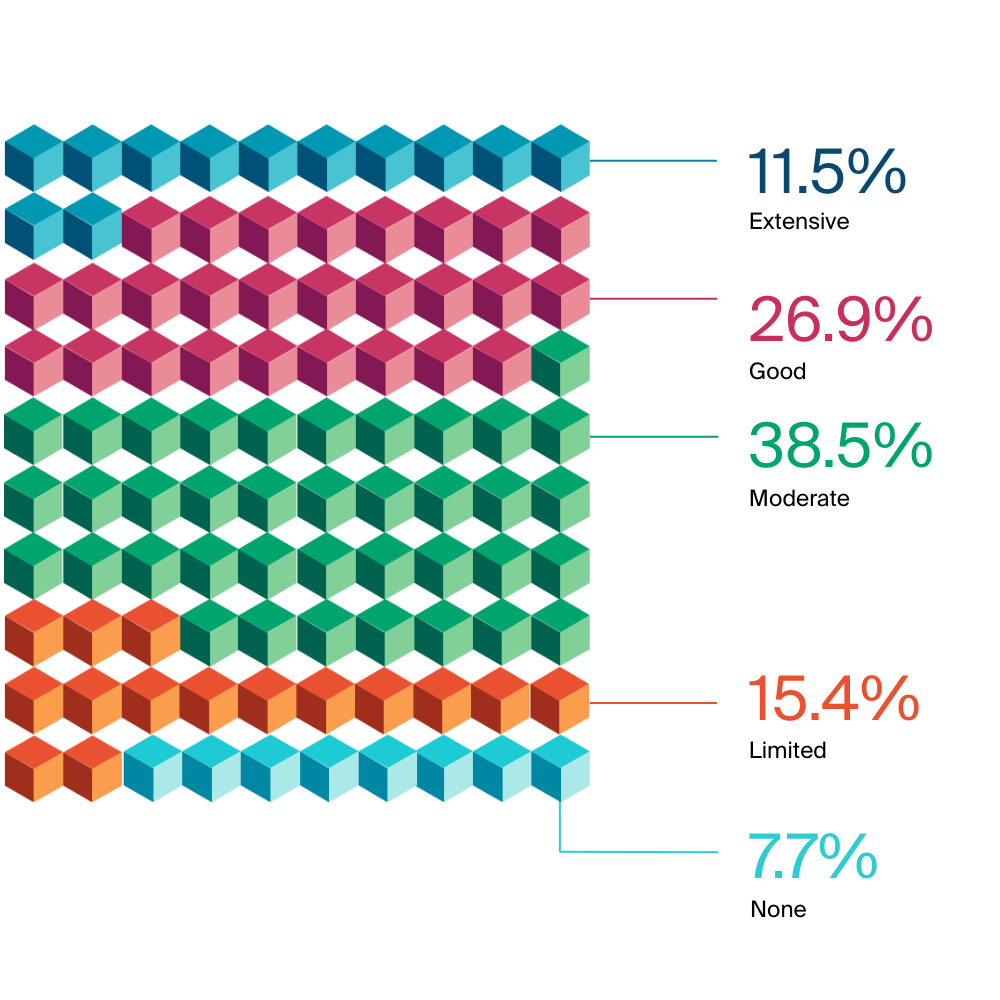

For over 15 years, corporate real estate has been told that ‘big data’ will change everything. Sensors, surveys, utilisation metrics, and workplace analytics have all been heralded as tools that would unlock new levels of insight and control. Yet despite the abundance of dashboards and reports, the question remains: how much of this data is actually being used to transform strategy and performance?

The hard truth is that data collection has outpaced data application. CRE leaders often sit on mountains of information, but translating data-driven insights into tangible change remains inconsistent. Dashboards do not cut costs, improve productivity, or enhance culture – decisions do.

This matters more than ever because real estate is now under heightened scrutiny. Space that sits empty or is visibly underused is no longer tolerated as a begnin inefficiency; it is increasingly seen as a liability. The financial pressure to justify cost, the cultural imperative to prove value to employees, and the sustainability demand to reduce unnecessary consumption all converge to put CRE leaders in the spotlight. Without a fact-based dialogue – grounded in credible data and visible action – leaders will be on the defensive. Worse still, they will find themselves unable to be progressive when it is most needed.

By % of respondents

The smart move is to shift from collection to transformation. Data needs to become the basis for decisive, fact-based conversations that remove emotion and sentimentality, and get to the truth of how space is used, what it costs, and how it enables business outcomes. This requires:

The discussion in Amsterdam brought some encouragement that this shift is underway. Dashboards for dashboard’s sake are being given a red light. It’s green for go on insights that shape action.

These six smart moves – moving upstream into strategy, acting decisively in volatility, rightsizing for alignment, relocating with purpose, ensuring the workplace performs, and turning data into action – capture the scale of the moment facing corporate real estate leaders. Each is urgent in its own right. Each is reshaping portfolios, workplaces, and strategies across the globe.

But beneath them lies an even harder truth. For all the recognition that real estate can drive business transformation, too many CRE leaders still face a brick wall regarding capital approval. The most imaginative strategies, the boldest relocations, and data-rich business cases mean little if the funding is not forthcoming. Without capital, the function is trapped in a cycle of efficiency-seeking, unable to deliver on its full potential.

That is why the defining challenge of this era is not just operational execution but financial elevation. CRE leaders must redouble their efforts to reframe real estate from a cost centre into a strategic investment – imperative for business transformation, central to achieving corporate ambitions, and critical to long-term competitiveness. This means articulating real estate’s role in growth, resilience, and culture in the same language boards and CEOs use to justify investments in technology, brand or M&A.

It is a defining period – but only if CRE leaders secure the resources to act. The opportunity is here now, while markets remain tilted toward occupiers regarding choice and cost. That window will not remain open indefinitely. When conditions harden, those who have failed to reposition real estate as a strategic investment will be unable to act precisely when action is most needed.

And that is where execution comes in. As arch-disruptor Elon Musk has said ‘Ideas are easy. Execution is everything.’ And in CRE, this means moving from plans to proof – winning the battle for capital, delivering outcomes at pace, and ensuring that real estate is recognised as a driver of growth and transformation.

Get the latest occupier trends and insights in your inbox.

(Y)our Space

Welcome to the fourth edition of (Y)OUR SPACE—Knight Frank’s global research campaign that explores the forces reshaping work, workplace, and the real estate strategies evolving in response.

01 December 2025

(Y)our Space

Findings from the latest (Y)OUR SPACE survey suggest that corporate real estate (CRE) is entering a defining phase—one shaped not by a single disruptor, but by a complex interplay of strategic, economic, and operational catalysts.

01 December 2025

(Y)our Space

The challenges facing corporate real estate.

01 December 2025

(Y)our Space

At the Sharp End: What CRE Leaders Are Telling Us About Supporting Growth and Transformation

01 December 2025

(Y)our Space

Portfolio in Motion: How Agility, Intelligence and ESG Are Rewriting Corporate Real Estate

01 December 2025

(Y)our Space

Pressure Points: The Top Challenges Shaping Workplace Strategy

01 December 2025

(Y)our Space

6 Hard Truths for CRE teams and the Smart Moves key to their future relevance and impact.

01 December 2025

Sorry!

An unexpected error has occurred.

Please try again later.