Over the next three to five years, occupiers are being compelled to make decisions in an environment marked by heightened uncertainty, innovation pressure, and evolving organisational models.

These themes echo—and intensify—the recalibrations first outlined in our Changing Tact report, where resilience and responsiveness were highlighted as emerging tenets of real estate strategy.

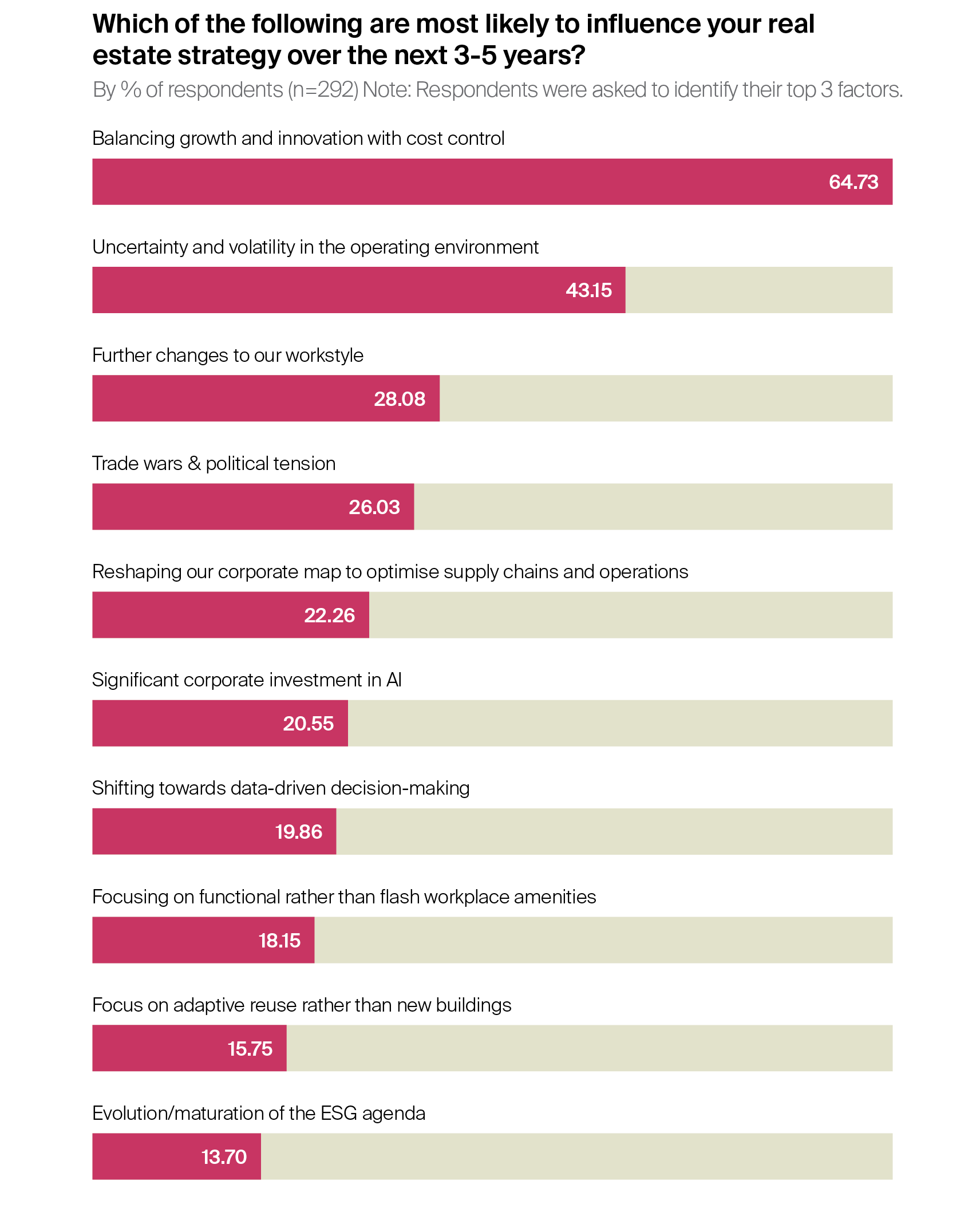

Taking the ten trends outlined in Changing Tact, we asked (Y)OUR SPACE survey respondents to identify the top three trends most likely to influence their real estate strategy out to 2029.

Topping the list of influences, selected by almost two-thirds of respondents, is the need to balance growth and innovation with cost control. This balancing act captures the essence of the current strategic moment: the ambition to modernise portfolios through technology and transformation is real, but must be tempered by cost discipline in a still-fragile and highly volatile macroeconomic environment. As Changing Tact noted, many occupiers are now applying a more forensic lens to space usage, prioritising return on investment (ROI) over presence.

Which of the following are most likely to influence your real estate strategy over the next 3-5 years?

By % of respondents (n=292)

Note: Respondents were asked to identify their top 3 factors.

The second most influential factor—uncertainty and volatility in the operating environment—cited by 43% of respondents, signals how deeply geopolitical and macroeconomic instability is shaping occupier sentiment. From inflationary pressures to geopolitical fragmentation, unpredictability has become a structural feature rather than a passing phase. In response, occupiers are embedding optionality and flexibility into their real estate strategies, favouring shorter lease terms, adaptable configurations, and going deep into scenario and contingency planning.

Workstyle evolution remains a key context-setting factor, selected by nearly 30% of respondents, making it the third most influential factor (although well short of the top two influences). As hybrid work settles into the mainstream, businesses continue to rethink how space can serve culture, cohesion, and performance. This reflects a shift from viewing the office as a static destination to considering it a fluid enabler of connection. Supporting this, 18% of all respondents also suggest a move toward functional rather than flashy workplace amenities will become more influential, perhaps indicating a return to purposeful design over prestige.

Operational and geopolitical catalysts also loom large. Trade wars and political tensions (26%) rank highly, just ahead of the connected drive to reshape corporate footprints to optimise supply chains and operations (22%). These results serve to reinforce the friend-shoring and regionalisation dynamics identified in Changing Tact, where occupiers expressed a growing need to align real estate footprints with strategic control and resilience. This has only heightened in significance in the early months of 2025.

Meanwhile, the emergence of AI and data-driven decision-making as mid-tier influences (21% and 20%, respectively) illustrates the accelerating push for intelligence-led strategy. As automation becomes more embedded in operations, real estate leaders are under pressure to translate data into insight—and insight into action. Analytics has never been more important.

As hybrid work settles into the mainstream, businesses continue to rethink how space can serve culture, cohesion, and performance. This reflects a shift from viewing the office as a static destination to considering it a fluid enabler of connection.

Notably, ESG was selected by just 14% of respondents, a sign perhaps of shifting focus in the near term. However, this may simply reflect prioritisation rather than disengagement. Changing Tact argued that sustainability remains woven into long-term strategy, even if it temporarily recedes behind more immediate imperatives and a changing political tone in some parts of the world.

Ultimately, responses to this fundamental and contextual question point to a period of transformation driven not by a single trend but by the convergence of many. This is a defining phase for corporate real estate—one where context matters as much as action and where the most successful strategies will be those able to integrate complexity, calibrate competing pressures, and stay focused on the road ahead.

How does this context translate into strategic priorities?

In a world still recalibrating from disruption, corporate real estate leaders are clearly facing a perfect storm of influences—economic volatility, geopolitical instability, digital acceleration, hybrid work, and rising ESG scrutiny. These aren’t passing headwinds; they’re structural shifts, reshaping the fundamentals of how, where, and why companies use space. In this new reality, real estate isn’t just a cost line or a backdrop to business—it’s a strategic platform for resilience, agility, and performance.

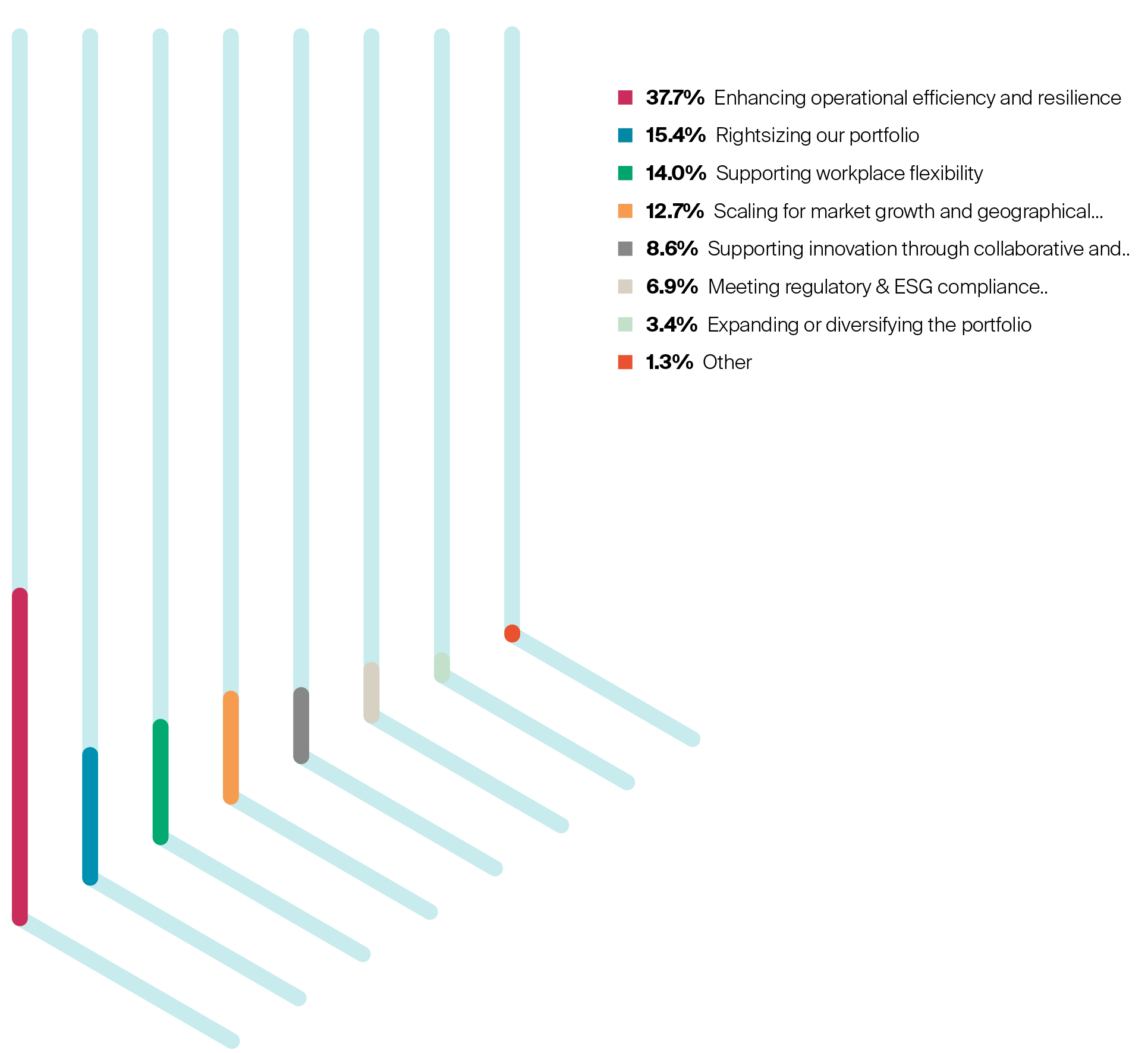

To understand how CRE leaders are responding to this challenging backdrop, the (Y)OUR SPACE survey also asked: "what is the primary goal of your real estate strategy over the next 3–5 years?" The results send a clear signal.

Enhancing operational efficiency and resilience topped the list by a wide margin, selected by 110 respondents—more than double any other category. This tells us the mood has shifted decisively. Occupiers are moving away from static space strategies and focusing instead on portfolios that flex, support continuity, and can absorb disruption without dragging down the business.

Secondary priorities reinforce this mindset. Rightsizing (45) and supporting workplace flexibility (41) come through as two sides of the same coin—both pointing to a recalibration of footprint and function in response to hybrid working. Further down the list, ambitions around growth, innovation, and ESG compliance remain in view, but they’re being weighed against the urgent need for stability and control. In short, real estate strategies are narrowing in on what matters most right now: resilience first, efficiency second, and everything else judged by how well it supports both.

What is the primary goal of your real estate strategy for the next 3-5 years?

By percentage of respondents (n=292)

But knowing the goal is only the start. Delivering on it means overcoming a series of structural, operational, and cultural challenges that are reshaping the role of CRE. In the sections that follow, (Y)OUR SPACE explores these challenges in detail—starting with the pressure to align real estate with business transformation agendas while managing risk and resource constraints. It then examines the realities of portfolio reconfiguration, from rightsizing and relocation to ESG integration and supply chain alignment. And finally, it takes a hard look at the workplace—where expectations are rising, utilisation has been falling, and the role of space is being redefined. Together, these three challenge areas reveal the scale—and the opportunity—of what comes next.