Business Growth & Transformation

At the Sharp End: What CRE Leaders Are Telling Us About Supporting Growth and Transformation

At the Sharp End: What CRE Leaders Are Telling Us About Supporting Growth and Transformation

As companies pursue growth against a backdrop of global disruption, the real estate function is increasingly expected to deliver more value, at greater speed, under more constrained conditions. It is being asked to reduce cost, mitigate risk, drive sustainability, enable transformation, and create places where talent can thrive — often without the access, influence, or internal alignment to do so effectively.

Knight Frank’s latest (Y)OUR SPACE survey offers a timely insight into what CRE leaders are experiencing on the ground. The responses reveal a function that is central to the future of business — but still wrestling with some fundamental constraints. What follows are six of the most significant challenges CRE teams are facing, as ranked by practising CRE professionals from across the world.

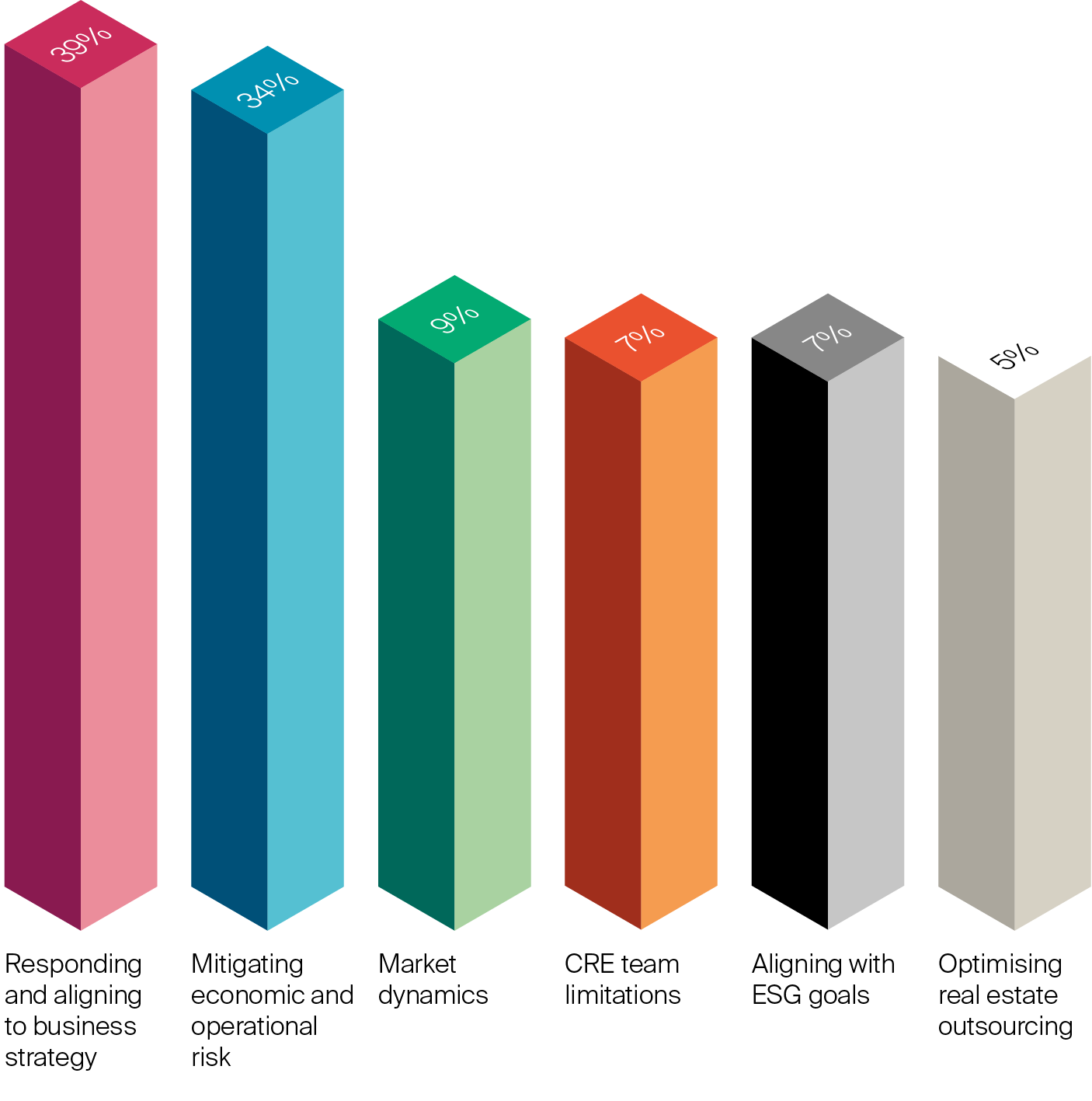

By % of respondents (n=292)

The most frequently cited challenge in the (Y)OUR SPACE survey - identified by 114 (39%) respondents - is the alignment of real estate with overarching business strategy. This certainly isn’t a new issue, but it has become much more urgent. As organisations pursue rapid transformation agendas around digital capability, M&A integration, decarbonisation and workforce reconfiguration, CRE leaders are being asked to deliver environments that enable these shifts - and often without the visibility, influence or lead time required to do so effectively.

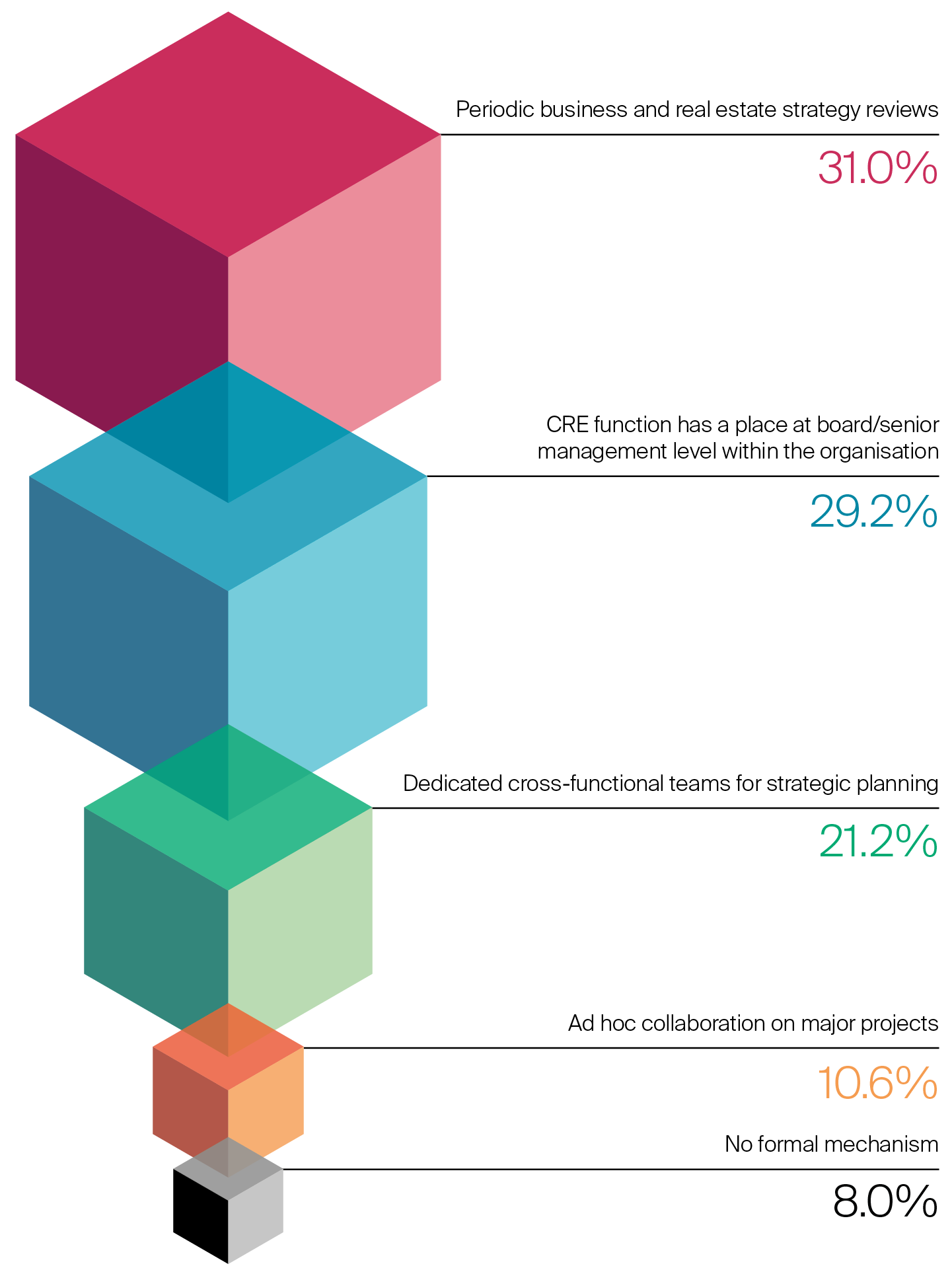

Too often, strategy is set before real estate enters the room. Athough 50% of respondents have either CRE representation at board level or a dedicated involvement in strategic planning, as many are more loosely aligned to business strategy either through reviews or ad hoc engagement. Worringly, eight per cent of all respondents had no formal engagement mechanism with the business at all.

By % of respondents (n=113)

These results suggest that too many CRE teams are brought in late, once decisions are already made, and asked to execute within boundaries they didn’t help define. This sequencing turns real estate into a response mechanism, not a strategic lever. The result is misalignment: space strategies that lag business strategies, and portfolios that fail to support emerging needs.

This lack of synchronisation carries material risks. Delayed alignment can lead to cost inefficiencies, operational friction, underutilised assets, or missed opportunities to support cultural or digital transformation. And in today’s more volatile context, with rising costs and compressed timelines, those missteps are harder to absorb.

What the data reveals is a growing recognition that CRE must be part of the strategic conversation from the outset. When brought in early, it can play a formative role: modelling future needs, flagging constraints, and ensuring that physical environments are designed to support rather than follow business direction.

Bridging the strategic gap isn’t just about better communication. It requires rethinking CRE’s internal mandate, elevating its visibility in enterprise planning, and giving it permission to challenge assumptions when necessary. The insight is clear: the earlier CRE is engaged, the more value it can unlock - for performance, for efficiency, and for resilience.

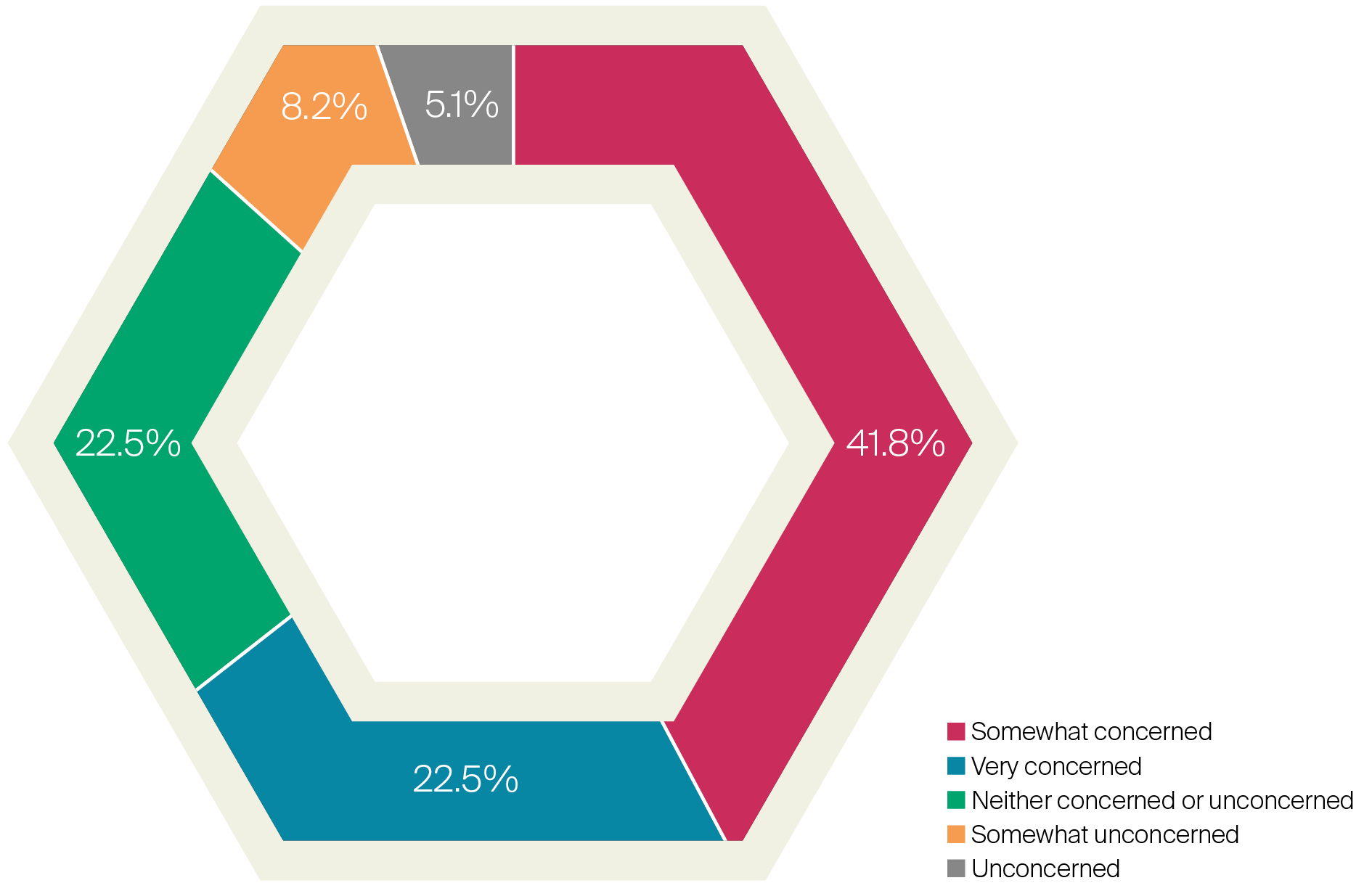

The second most commonly cited challenge, reported by 98 (34%) respondents, is managing operational and economic risk in a context where volatility appears to be the new normal. CRE teams are operating without the buffers they once relied on: timelines are tighter, cost predictability is low, and flexibility is expected across every lease, layout and investment decision. Sixty-three per cent of respondents were either ‘very concerned’ or ‘somewhat concerned’ about the impact of economic volatility on their medium-term CRE strategy.

By % of respondents (n=98)

Macroeconomic shifts are only one part of a broader, more complex risk environment. They also reflect operational realities, such as changing patterns of demand, high energy costs, geopolitical uncertainty, supply chain disruption, and ongoing pressure to right-size portfolios. In this context, CRE is being asked to offer optionality and resilience while still delivering efficiency.

The challenge is not simply one of mitigation. It’s about enabling decision-makers to move forward confidently, even when the outlook is uncertain. That places new emphasis on data, scenario modelling, governance agility, and real-time portfolio visibility - capabilities that many CRE functions are still developing. Survey responses suggest a shift in how risk is understood: not just as something to defend against, but as a condition to work through. For CRE leaders, the task now is to protect the organisation from downside exposure without slowing its capacity to act.

Perhaps the biggest shift is a recognition that economic and operating risk is high and will remain so, meaning that it is no longer sufficient to simply apply the brakes and buy-time. Volatility and uncertainty is a business reality, and managing against it is an imperative even if traditional buffers no longer-exist.

Selected by 26 (9%) respondents, market conditions emerged as another significant friction point. CRE strategies - no matter how well aligned or urgent - must still be delivered through real-world constraints. And those constraints are shifting fast.

Survey respondents pointed to rising construction costs, supply chain delays, limited availability of prime space, and the challenges of securing compliant, future-ready buildings in key locations. At the same time, business expectations have sped up. Timelines are tighter, fit-outs are under greater scrutiny, and hybrid working has made space needs more fluid but not necessarily more flexible.

This creates a disconnect: organisations want to move fast, but market conditions are slow, unpredictable, or uncooperative. Even when the strategic intent is clear, execution can falter due to external realities.

CRE teams are adapting: exploring shorter leases, more modular layouts, and phased delivery models. But these are workarounds, not structural solutions. Until market supply and demand rebalance, this will remain a constraint that even the best strategies must learn to navigate.

While only 20 (7%) respondents selected capability constraints as their primary challenge, the issue of team capacity, skills and structure surfaced repeatedly throughout the survey. In many organisations, the scale of expectation now firmly outpaces the resourcing of the CRE function.

CRE leaders are being asked to support workplace transformation, ESG delivery, portfolio optimisation, digital reporting, and strategic planning - often with small teams, legacy systems, and limited bandwidth. In some cases, responsibility has grown faster than capability development. In others, and as noted, real estate still operates on the margins of enterprise decision-making, without the visibility or access needed to truly lead.

This tension is not about competence, it’s about calibration. Today’s CRE mandate requires a different operating model: broader skill sets, stronger integration with other corporate functions, and greater investment in both people and platforms.

Organisations that fail to evolve the structure of the CRE function risk overburdening or, worse, underutilising it. Those that invest in capability will be better placed to harness CRE as a driver of business performance, not just a cost centre.

Sustainability and ESG alignment was cited by 20 (7%) respondents - fewer than other challenges, but still firmly on the radar. What’s notable is that for many organisations, sustainability is no longer treated as a discrete issue. Instead, it is embedded across decisions, designs, and expectations.

For CRE leaders, this means every lease, fit-out, refurbishment, and procurement decision is now a sustainability decision. Operational performance is tracked, targets are public, and carbon is being counted. Investors, regulators, and employees all expect visible progress, and fast.

The challenge of the next three years is less about intention and more about execution. Many corporate net zero targets are pinned to 2030 - now just five years away. Yet most corporate portfolios include legacy buildings, long leases, and limited flexibility.

CRE teams are therefore delivering change at the edge of what they can directly control - nudging landlords, retrofitting old stock, and trying to move the dial within rigid frameworks. The sustainability conversation has matured. But the delivery challenge is only just beginning.

Fifteen respondents (5% of the total) identified the optimisation of real estate outsourcing as their top challenge and while the number is lower than other categories, the issue has wide-reaching implications.

As demands on the CRE function grow, so too will its reliance on external partners to scale delivery, extend geographic reach, and provide specialist expertise. But many survey respondents pointed to variability in service quality, accountability, and cultural alignment, particularly across large, complex portfolios.

The outsourcing model that once delivered operational efficiency now faces a more complex brief: support innovation, adapt to change, and operate as a seamless extension of the client’s internal team. That requires more than contracts: it requires trust, transparency, and shared purpose.

CRE leaders are looking for more agile, strategic partnerships. Providers who can flex with shifting requirements, co-create solutions, and help deliver more than just square footage. The goal isn’t simply to outsource, it’s to collaborate.

The picture that emerges from this first challenge area is not one of a function in crisis, but one in transition. CRE teams are no longer being asked to just manage space - they are being asked to drive transformation. That shift comes with pressure, friction, and structural misalignment. But it also comes with tremendous opportunity.

To meet rising expectations, organisations must evolve how they position, resource, and empower their real estate functions. That means granting earlier access to strategic planning, investing in talent and systems, reforming legacy governance models, and selecting partners who can flex with complexity.

Above all, it means treating CRE as what it has become: a strategic platform for business performance. CRE leaders aren’t waiting for permission to lead, they’re asking for the conditions to do it well.

Get the latest occupier trends and insights in your inbox.

(Y)our Space

Welcome to the fourth edition of (Y)OUR SPACE—Knight Frank’s global research campaign that explores the forces reshaping work, workplace, and the real estate strategies evolving in response.

01 December 2025

(Y)our Space

Findings from the latest (Y)OUR SPACE survey suggest that corporate real estate (CRE) is entering a defining phase—one shaped not by a single disruptor, but by a complex interplay of strategic, economic, and operational catalysts.

01 December 2025

(Y)our Space

The challenges facing corporate real estate.

01 December 2025

(Y)our Space

At the Sharp End: What CRE Leaders Are Telling Us About Supporting Growth and Transformation

01 December 2025

(Y)our Space

Portfolio in Motion: How Agility, Intelligence and ESG Are Rewriting Corporate Real Estate

01 December 2025

(Y)our Space

Pressure Points: The Top Challenges Shaping Workplace Strategy

01 December 2025

(Y)our Space

6 Hard Truths for CRE teams and the Smart Moves key to their future relevance and impact.

01 December 2025

Sorry!

An unexpected error has occurred.

Please try again later.