Nerves and mortgage rates take time to settle in prime London property markets

November 2022 PCL sales index: 5,450.7

November 2022 POL sales index: 276.8

2 minutes to read

Rishi Sunak may have become Prime Minister six weeks ago, but the UK housing market is still living with the repercussions of the mini-Budget that took place a month earlier.

The financial shockwaves are dissipating as the Christmas break approaches, making it difficult to assess how much damage was ultimately done.

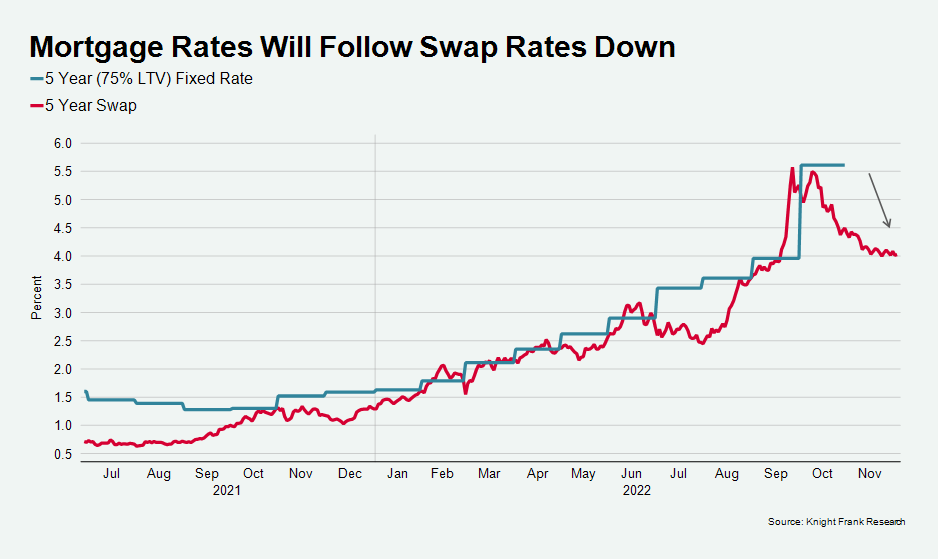

The inflationary potential of the low-tax economic plan set out by former Chancellor Kwasi Kwarteng alarmed financial markets and sent interest rate expectations higher. Mortgage rates spiked but have started dropping as swap rates return to where they were before the mini-Budget.

We expect mortgage rates to edge down as lenders increasingly price mortgages based on lower swap rates, see chart.

Prime London markets are more protected from this financial pain, but they are not immune.

Prime central London (PCL), in particular, benefits from a higher percentage of cash buyers than prime outer London (POL), which will underpin demand and prices.

For example, activity in the £10 million-plus super-prime market is currently robust, as we explore here.

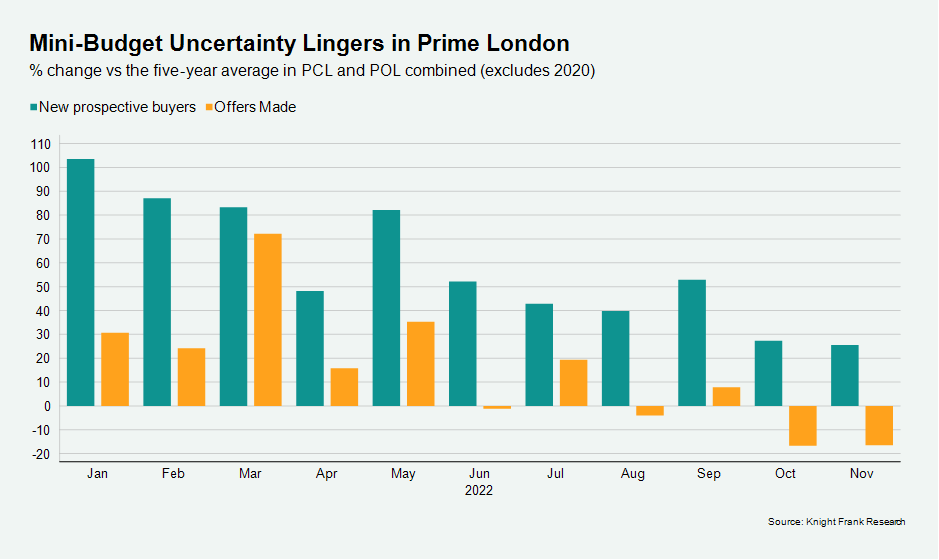

In the wider prime market in London, demand is still relatively strong, but the recent mortgage market volatility has led to fewer offers being made.

While the number of new prospective buyers was 26% above the five-year average in November (excluding 2020), the number of offers made was 17% lower. Meanwhile, on the supply side, the number of new sales instructions was 5% higher.

The figures point to the understandable anxiety felt by buyers but don’t show a notable fall in demand. In other words, buyers are hesitant but haven’t disappeared.

Prices in prime London postcodes dipped for the second consecutive month, mirroring the wider UK market.

Average prices in PCL fell 0.2% in November, taking the annual change to 1.7%. In POL, the decline was 0.1%, which produced an annual increase of 4.6%.

We don’t expect the kind of cliff-edge moment for property markets seen during the financial crisis next year, for reasons explored here. Our latest forecast for prime London markets is here.

It is logical that the financial pain will spread further after Christmas as more pre-mini-Budget mortgage offers lapse. However, the pain should also be less acute as rates and nerves begin to calm back down.