Which UK areas have the highest % of cash buyers?

Some parts of the country may be more insulated from rising mortgage costs than others

3 minutes to read

In the same way the pound became a barometer for sentiment following the Brexit vote, the swap market is providing a verdict on the new government’s economic plan.

In simple terms, swap rates have risen because financial markets believe the Bank of England will have to raise rates more aggressively to contain inflation following the tax cuts announced in last month’s mini-Budget.

That matters to households because fixed-rate mortgages will also increase. More than 95% of mortgage lending since 2019 has been on a fixed rate.

And it matters to the government because if people are paying notably higher mortgage costs, this would overshadow its tax giveaways and hurt its chances at the next election.

It is a chain of logic that makes the current situation feel untenable, as we explored here. Recent jitters in the gilt market have piled further pressure on the government.

The five-year swap rate was almost 5.5% in the second week of October, which compares to 3.9% in mid-September. As a result of this changing rate environment, we have revised down our forecast for the next two years.

Higher lending rates have so far led to mixed fortunes in the housing market.

Anyone coming to the end of a fixed-rate term or buyers with a lapsing mortgage offer are at the sharp end of what is taking place.

As more buyers come up against the reality of monthly mortgage bills rising by hundreds of pounds, the financial pain will spread through the housing market.

Against a backdrop of rising borrowing costs, one variable to consider will be housing equity. Cash buyers and those using low levels of debt will be comparatively less exposed to the vagaries of the mortgage market.

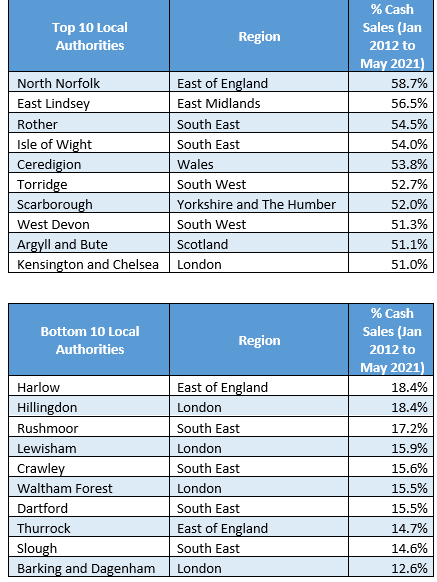

Buyers in outer London and parts of the south-east areas have typically relied most on mortgage debt in the UK, an analysis of Land Registry data since 2011 shows. Cash buyers have accounted for less than 20% of sales in areas including Barking and Dagenham, Slough, Thurrock, Dartford and Waltham Forest. The UK average was 31%.

Meanwhile, the list of areas where cash buyers are most prevalent has a distinctly second-home feel and is topped by the coastal areas of North Norfolk (59%), East Lindsey (57%) and Rother (55%). Relatively higher levels of retiring homeowners are also likely to have affected the figures.

Inside the capital, Kensington & Chelsea (51%), the City of London (47%) and Westminster (46%) have led the way for cash buyers over the last decade. Prime central London will be further boosted by returning international buyers and a weak pound, as we explored here.

“The more equity that flows into and is already inside a particular housing market, the lower the level of financial distress,” said Tom Bill, head of UK residential research at Knight Frank. “Downwards price pressure will be felt everywhere but some locations will be more insulated than others.”

More widely, record low UK unemployment and the fact lenders are well-capitalised and reportedly looking at forbearance options for borrowers will also help contain the type of forced selling and double-digit annual declines seen during the global financial crisis.