Rate hike is latest signal that UK house prices will cool

What’s more open to debate is how steeply or quickly the housing market will moderate.

3 minutes to read

The fourth consecutive base rate rise last month had a noticeable impact on the UK property market.

More sellers came forward in the belief that the market may be peaking, many no doubt prompted by the vivid language used by the Bank of England to downplay the prospects for the economy.

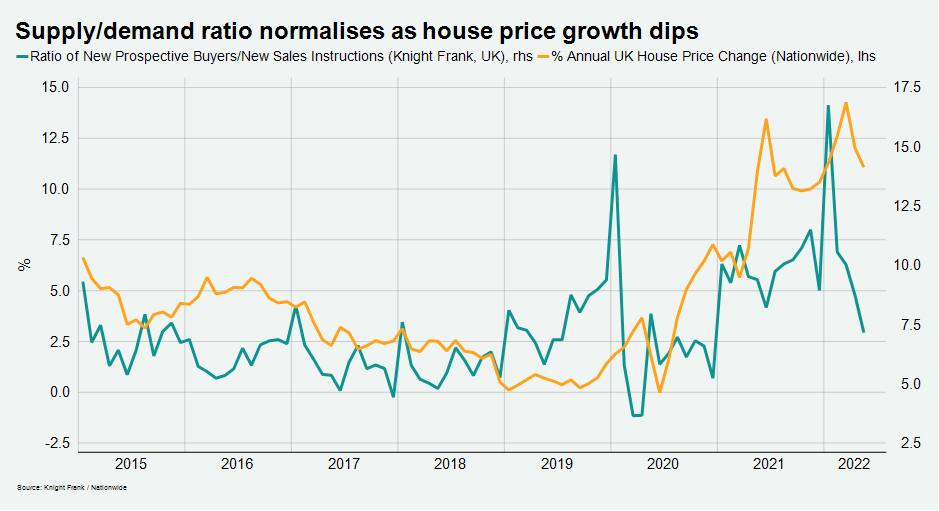

The number of UK sales instructions in May was the fifth highest monthly total in a decade, having jumped 35% from April. The ratio between new sellers and buyers also approached its longer-run average of between 6 and 7 last month, as the chart below shows.

Following the fifth consecutive rise in the base rate to 1.25% from 1% this week, it’s a reasonable assumption that supply will continue to build and put more downwards pressure on prices.

Last month’s dip in demand versus supply followed a surge over the last 18 months, magnified by the stamp duty holiday that ran for 14 months from July 2020.

However, it isn’t just a UK phenomenon. The US is currently seeing a so-called ‘real estate refresh’ after a similar period of weak stock levels.

“The latest interest rate rise will accelerate the process of normalisation taking place in the UK housing market,” said Tom Bill, head of UK residential research at Knight Frank. “Unlike other parts of the economy, we don’t expect decades-old records to be broken in the property market and prices will continue to drift back down to earth after the distortions of the pandemic.”

Any moderation in prices won’t just be the result of more sales listings, however.

Lenders are currently pulling their cheapest mortgage products on a weekly basis and sometimes more frequently, according to Simon Gammon, head of Knight Frank Finance.

“Buyers may not appreciate quite how much the mortgage market has moved in the last four to six weeks,” said Simon. “They may have a particular property in mind based on research done earlier this year, but rising rates mean it could now be unaffordable. This effect will naturally keep prices in check.”

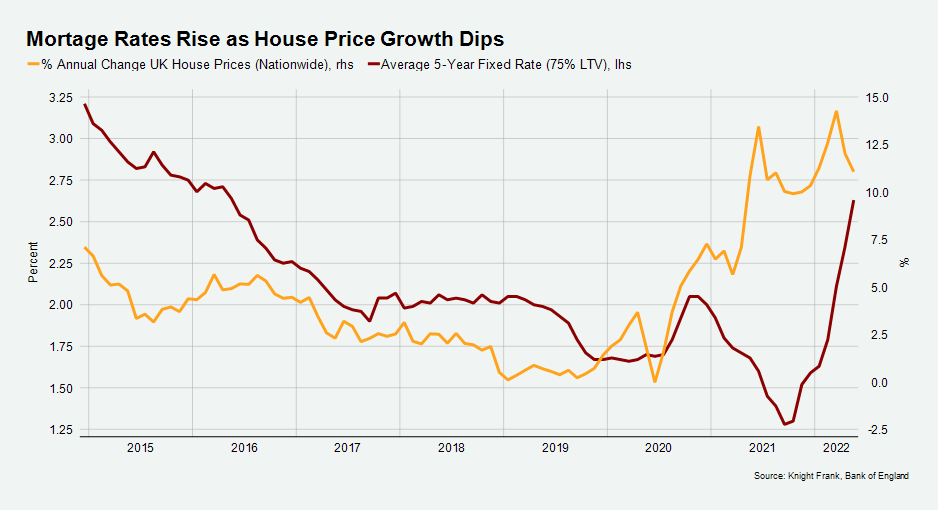

The average cost of a five-year fixed-rate mortgage on a 75% loan-to-value basis in May was 2.63%, more than double the figure of 1.7% last May, as the chart shows. On a £250,000 mortgage, the extra interest payments over the five-year fixed period would be close to £12,000.

A desire to act before the market begins to tail off is one of the reasons activity is currently so strong in London and the rest of the UK.

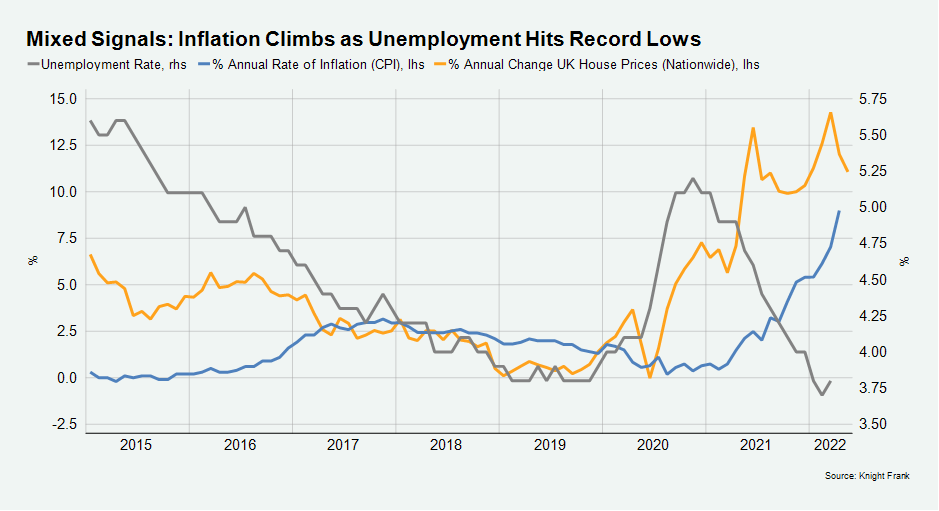

There is also a cost-of-living squeeze to factor in. We may be near a point when the rate of inflation exceeds annual house price growth, as the chart below shows. Low unemployment means we don’t expect growth to start falling and our latest forecast can be found here.

The direction of travel for house prices is clear. What’s more open to interpretation is how prolonged or rapid the decline in growth will be, particularly during a disorientating period when inflation is at its steepest in 40 years, unemployment is at a 48-year low and interest rates are at a 13-year high.