Slow Recovery for UK Housing Market as it Awaits Political and Economic Clarity

Recent indicators suggest transaction volumes are rising as spring approaches but the pressure on pricing is downwards.

3 minutes to read

It feels as though the UK housing market is waiting for something to happen.

The prevailing mood is one of anticipation with both a rate cut and a new Prime Minister on the horizon.

Even recent house price data suggests the current direction of travel is sideways. The monthly growth reported by Nationwide and Halifax in the first two months of the year went into reverse in March.

Frustratingly for buyers, the prospect of the first rate cut since March 2020 seems to move further into the distance with each release of economic data.

Figures from the US have recently caused concern due to a belief the Bank of England won’t cut rates before the Federal Reserve.

Strong US inflation figures sent the UK five-year swap rate above 4.3% last week, which is clearly not good news for anyone hoping to agree a mortgage starting with a ‘3’ any time soon.

The fact a wave of borrowers are rolling off sub-2% fixed-rate mortgages agreed at the start of 2022 is adding to the financial pressures in the system, as we explored here.

More relief for buyers will come when underlying inflation appears to be under control, so watch the UK numbers closely on Wednesday.

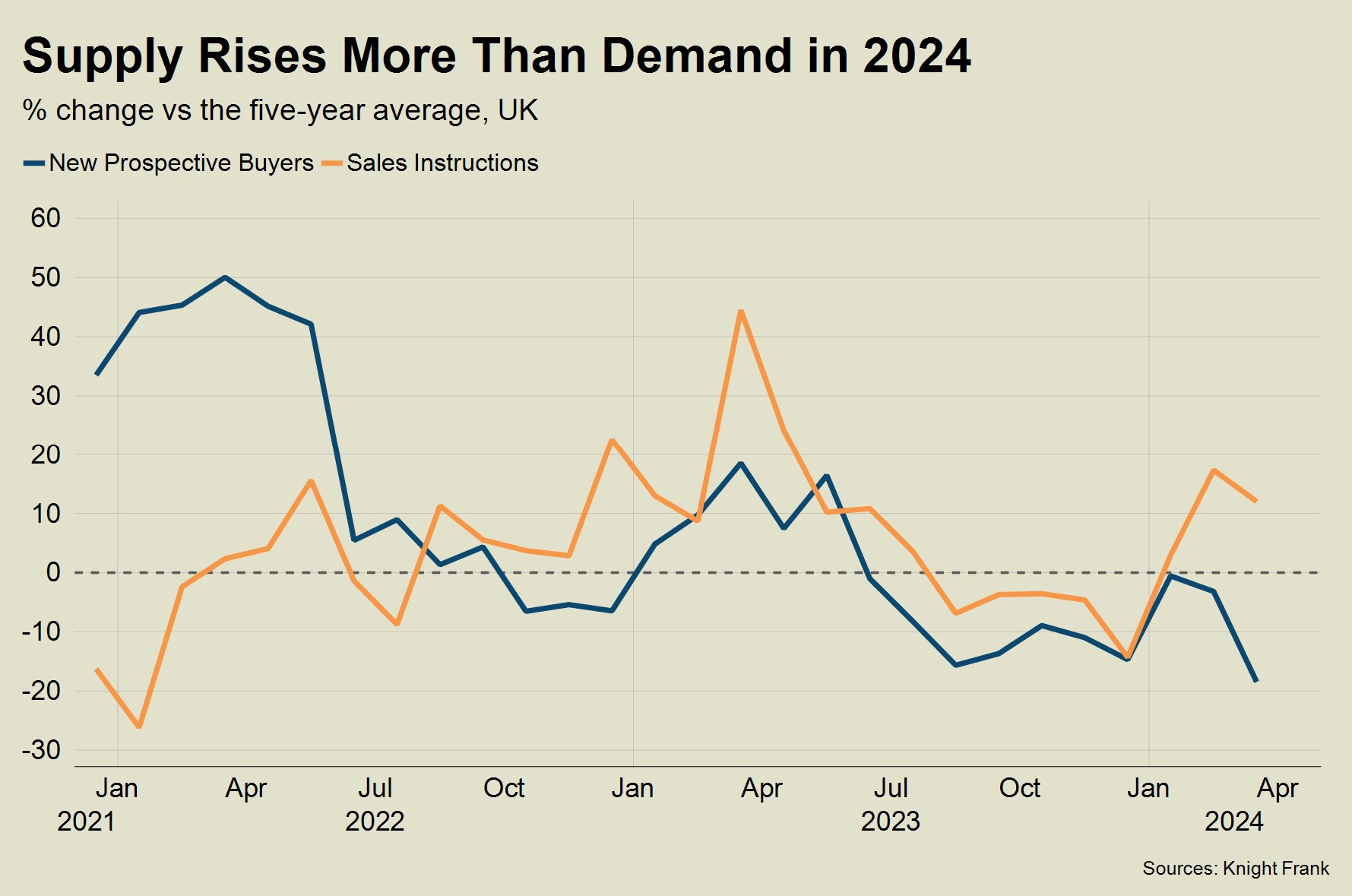

The other reason prices are dipping is rising supply. The positivity that infused the market in the early weeks of this year means more properties are now coming onto the market.

The latest RICS report shows that supply has risen for four consecutive months, which tallies with Knight Frank data. A dip in demand in March is also visible due to mortgage rates creeping higher.

With more properties on the market, it is reasonable to expect a seasonal bounce in activity this spring. Indeed, mortgage approvals hit a 17-month high in February.

Playing Politics with Tax

While anyone buying or re-mortgaging waits for better news on rates, the higher-value end of the property market was recently reminded of the upcoming election.

We recently explored how transactions in south-west London have been supported by the greater proportion of buyers moving for work or schooling. Meanwhile, higher-value markets in prime central London, where demand is typically more discretionary, have seen more indecision due to stubbornly-high borrowing costs.

Any hesitation has no doubt been exacerbated by uncertainty over the non-dom tax changes announced by Jeremy Hunt in early March.

Under previous rules, non doms did not pay UK tax on foreign income but the government plans to restrict such benefits under a more transparent system.

Now, the Labour Party says it would fund health and education pledges by making the rules even tighter.

It feels like an appropriate moment to mention the ‘Laffer Curve’ - an economic theory that suggests overall revenue falls when the tax rate is too high.

Beyond the headlines and political one-upmanship, both parties may want to carefully consider the ideal tax rate to maximise revenue from the UK’s 69,000 non doms to fund important political projects. Or that the anticipated revenue may not be achieved if enough non doms leave the UK.

But then again, maybe this sort of pragmatic thinking can only come after a general election? By which stage it is hopefully not too late.