Prime London Rental Values Retreat as Supply Builds

February 2024 PCL lettings index: 219.7

February 2024 POL lettings index: 220.9

3 minutes to read

Seasonality is returning to the prime London lettings market after three tumultuous years.

The pandemic meant the market was initially flooded with stock in 2020 as short-lets were banned under Covid rules. Then, once the sales market ignited due to a stamp duty holiday and the ‘race for space’, it prompted more landlords to leave the sector because of the growing regulatory and tax burden.

Now, as supply gradually rebuilds and demand cools, it has pushed rental value growth down in recent months, as we have previously explored.

Average rents in prime central London rose 6.3% in the year to February, which is a threefold decrease from the 18% recorded in the same month last year.

In prime outer London, average rents increased 5.5% in the year to February, which is also not far off a threefold decrease versus 15.6% twelve months ago.

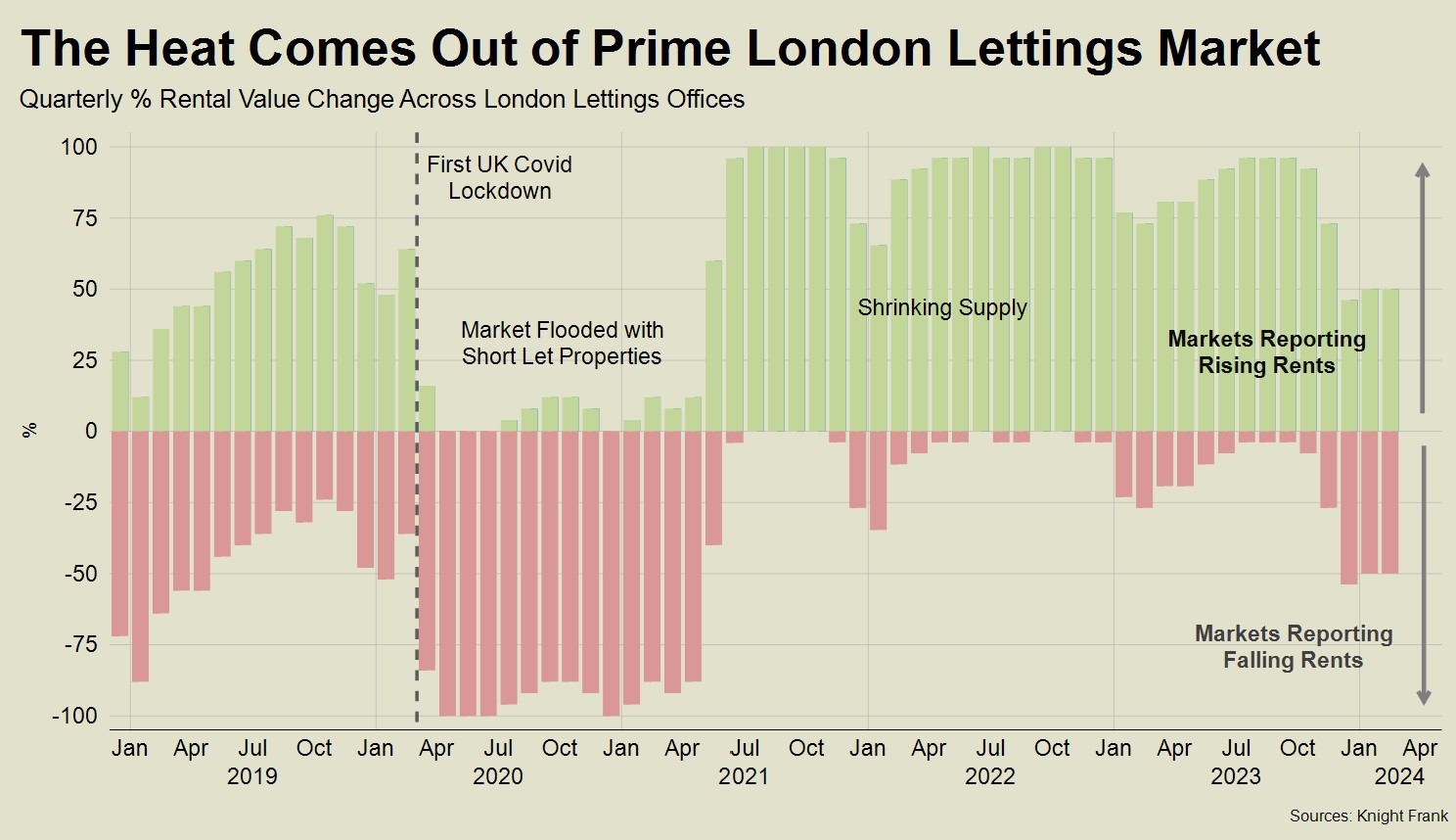

This return to more normal conditions after the pandemic can be seen on the chart below.

It tracks how many London areas are experiencing a quarterly increase in rental values versus a decline.

While 2020 was marked by widespread rental value falls as supply spiked, the following two years saw strong growth as supply retreated. New listings were down by around a third during much of 2021 and 2022, while the number of new prospective tenants registering with Knight Frank in London was up by a similar amount.

Rental value growth across London as a whole tends to be weaker in the first quarter due to the pattern of the academic year, as the chart shows. That seasonality is returning in 2024.

It’s also true that the supply of higher-value rental stock has risen more due to the fact owners are more discretionary and have opted to let rather than sell while price growth was weak in recent months, as we have previously analysed.

Despite this return to more balanced conditions, Chancellor Jeremy Hunt used this month’s Budget to encourage more landlords to sell by reducing the rate of capital gains tax on residential property to 24% from 28% in April.

Depending on their taxable gains, it may tip some into selling. A full Budget analysis can be found here on the implications for the UK residential market.

As more balance returns, some parts of the capital saw a modest annual decrease in rents in February, such as Wapping (-0.3%), South Kensington (-0.5%) and King’s Cross (-0.1%).

All three areas have experienced their own unique supply and demand dynamics.

Wapping has seen demand fall compared to the City and Aldgate, which are targeted by students, said Marie Wale, head of lettings at Knight Frank’s Wapping office. “In the financial services market, a lot of tenants are choosing to live close to work in Canary Wharf,” she said.

Meanwhile, demand has become softer in King’s Cross among Asian students, including those from mainland China, said David de Almeida, a senior lettings negotiator in the Knight Frank King’s Cross office.

UK universities may have reached “peak China”, according to recent comments from the head of the Universities and Colleges Admissions Service, for reasons that include recent visa and tax changes.

And South Kensington has seen higher levels of supply push rental values down, according to Mark Batty, head of lettings at the Knight Frank South Kensington office.

“Most things are renting at under the asking rent,” said Mark. “About three-quarters of our available properties are above £1,000 per week and more owners are deciding to let them out after failing to sell.”