Is it time to simplify ESG investment?

With this increasingly coalescing around environmental sustainability, we ask whether a stripped-down investment framework might make for more successful outcomes.

4 minutes to read

As every investor must by now be aware, ESG brings together three distinct investment criteria: E represents environmental themes; S considers social outcomes; while G looks at governance issues.

From an investor perspective, the rapid evolution of environmental regulation in the US, EU and the UK confirms the need to focus on the E aspect of their portfolios.

This is not true to anything like the same degree for the S and the G. The 2020 complaint from Hester Peirce, Commissioner on the US Securities and Exchange Commission, that “ESG is broad enough to mean just about anything to anyone...and...allows experts great latitude to impose their own judgements, which may be rooted in nothing at all other than their own preferences” still seems a fair challenge in relation to the latter two areas of ESG.

As environmental requirements for buildings and investments become increasingly codified, the benefits of bundling S and G into the mix become more debatable. Isn’t there a potential win to be gained from simplifying the investment objectives of ESG and, as The Economist argued last year, supercharging the impact of environmental improvements through a relentless focus on E – redefined to mean “emissions” rather than the broader spread of topics implied by the more loosely drawn term “environment”?

Our research into private investor objectives suggests there may be some justification for this approach. In The Wealth Report in 2021 we revealed that while six in ten ultra-high-net-worth-individuals (UHNWIs) felt they lacked the information they needed to assess ESG-related investments, 43% were increasingly interested in compliant investment opportunities.

The key driver behind this ESG investment push, as we revealed in our 2022 report, was future-proofing portfolios, but even with this rationale almost half of investors stated that finding the right opportunity was a barrier.

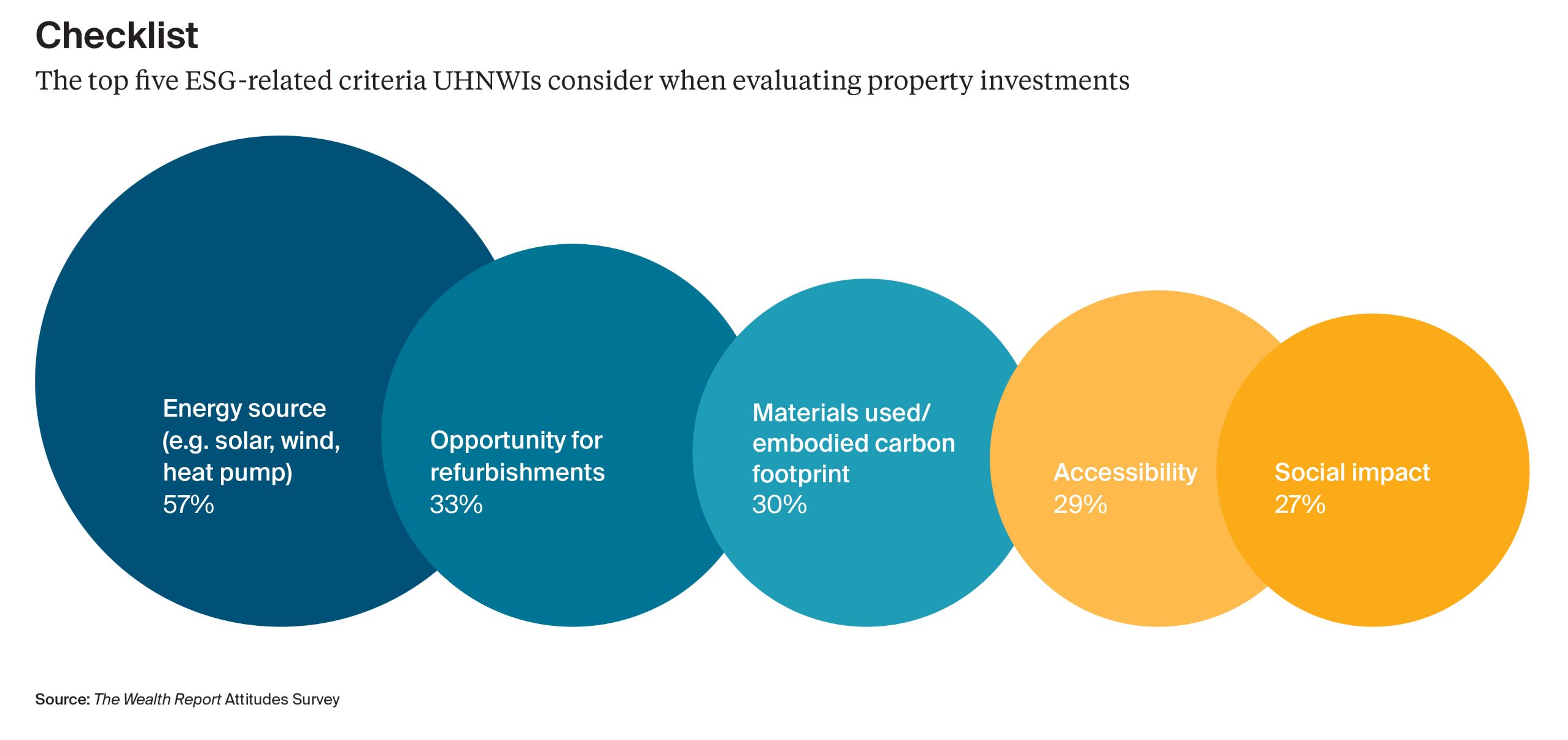

This year our Attitudes Survey results, based on responses provided during November 2022 by more than 500 private bankers, wealth advisors, intermediaries and family offices revealed in January’s Outlook Report 2023, took the analysis deeper, allowing us to understand which ESG-related criteria UHNWIs are considering when investing in property.

The results showed that energy source (57%), opportunities for green refurbishments (33%) and materials/embodied carbon (30%) are increasingly being factored into the decision-making process. When we asked about the leading risks and opportunities relating to the ability to create and grow wealth, energy and climate issues were cited as both.

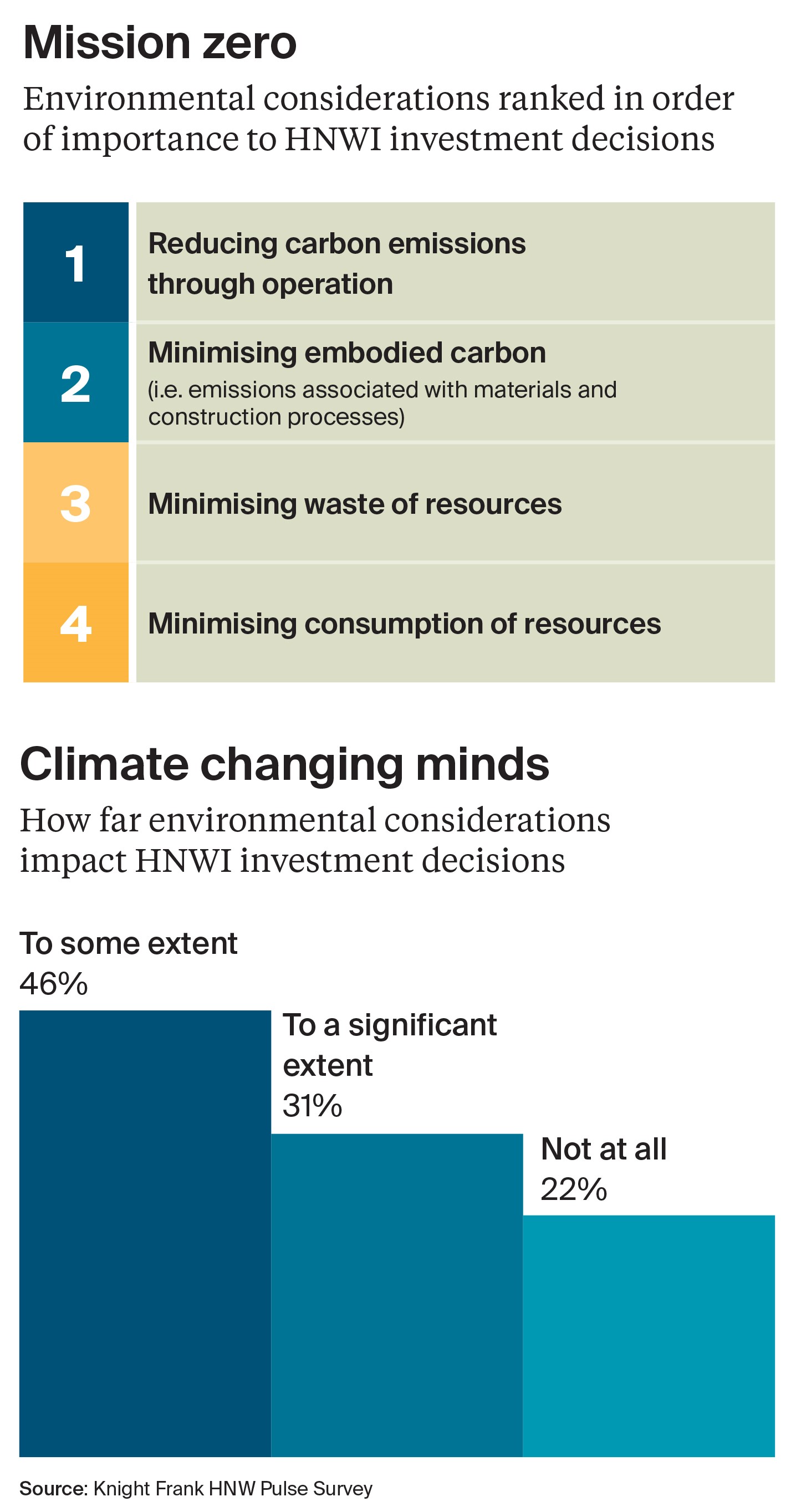

These findings are reinforced by our high-net-worth Pulse Survey, capturing the views of 500 HNWIs across ten countries and territories, which confirms that environmental considerations impact investment decisions for nearly four-fifths of investors. The results again clearly point towards carbon emissions as the leading environmental investment consideration.

It seems clear from our research that the E in ESG dominates in terms of investor interest. In the Attitudes Survey, the three top-performing criteria all related to environmental issues, ahead of social criteria such as accessibility. The G doesn’t even get a look in.

This reticence may stem from concerns such as those raised by Hester Peirce. The past 12 months illustrate the challenges involved in trying to identify good and bad investment practice from a social and governance perspective.

In February 2022, if you leased R&D space to an arms manufacturer some fund managers would have considered you beyond the pale; do the same a month later and the Ukraine crisis meant you were beyond reproach.

What about S and G?

Investors may regard the increase in environmental regulatory requirements with trepidation, as businesses set about scaling up their compliance teams to report on their scope 1, 2 and 3 carbon emissions. That means all the emissions a company makes directly; all those it makes indirectly; and all those it causes its suppliers to make and that customers make when using its products or services.

It sounds like a significant challenge, but at least E has a decent primary target – to reduce carbon emissions.

But who sets the objectives and defines the standards for S and G? Is providing retail property a social benefit? Is real estate dedicated to employment better for society than that dedicated to housing? Should investors be prioritising diversity at board level, or accessibility in early careers?

None of this means an investor shouldn’t prioritise the delivery of, say, affordable housing if they see a business opportunity, or if it fulfils a personal or investment goal – but ESG criteria may not be the best guide to aid this decision making process.

With most private investors confirming an interest in environmental objectives, and with this being reinforced by regulation, and with the S and the G remaining less codified and subject to shifting notions of what makes an appropriate target, simplifying ESG may be the best way to help meet private investors’ primary non-financial objectives.

Discover more

Download

Download the full report for more in depth analysis and the latest trends relating to global wealth.

Download the report

Subscribe

Subscribe for all the latest insights and additional content.

Subscribe