The UK economy shrinks

Making sense of the latest trends in property and economics from around the globe.

4 minutes to read

The UK economy shrinks

UK GDP contracted 0.1% during the second quarter, according to a preliminary estimate from the ONS out this morning.

There are good reasons to take the reading fairly lightly. The contraction accelerated at the end of the quarter, with output shrinking 0.6% in June, though there were fewer working days due to the Jubilee. Services led the contraction, declining by 0.4%, but that was largely due to falling human health and social work amid falling Covid-19-related activities. Bright spots included tourism amid the easing of restrictions, plus accommodation and food services, arts, entertainment and recreation.

Much of that should be corrected in the coming quarter so is unlikely to deter the Bank of England's Monetary Policy Committee from its commitment to rein in inflation.

Demand for housing falls

Rising house prices underpinned by stock levels close to all-time lows - that much about July's RICS Residential Market Survey looked the same as the many months that preceded it.

All metrics of demand and activity are now in negative territory, however. New buyer enquiries came in with a net balance of -27% and contracted in every region. That metric has posted negative readings on a national basis for three straight months, the longest stretch of falling demand since the onset of the pandemic. Agreed sales posted a reading of -13%, largely flat on the previous month. Near-term sales expectations fell to -20%, from -11% last month. Sales expectations at the twelve-month horizon fell to -26%, down from -21% last month, the most downbeat figure since March 2020.

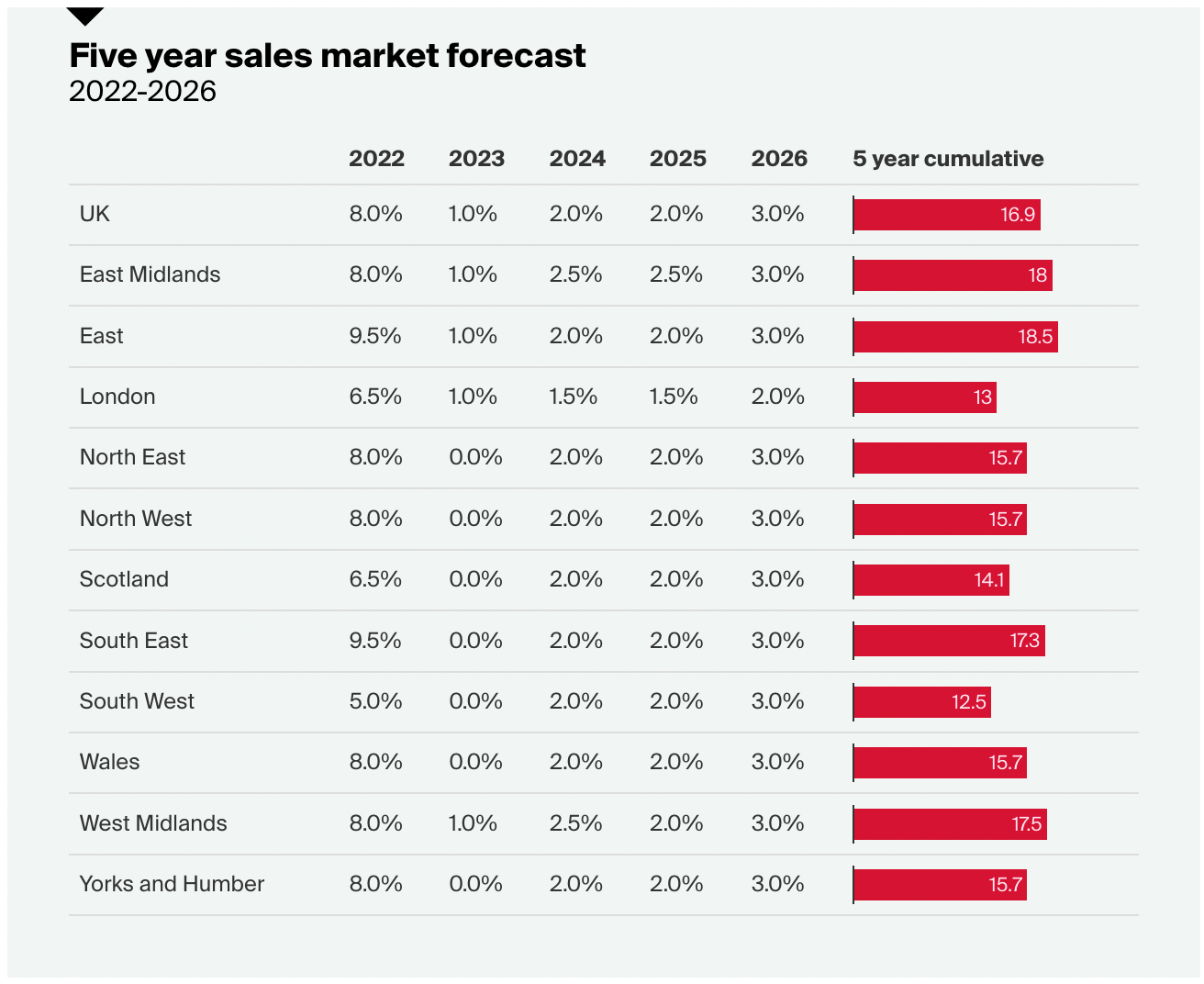

Where do we go from here? Many people are taking their first holiday in two years, which is contributing to a particularly slow summer from a supply perspective. That should pick up in line with the usual seasonal patterns we see during the Autumn. We maintain our view that house prices will cool to close the year in single digits - see our forecasts here and the chart below.

The hottest global markets cool

Housing markets that saw the most rapid rates of price growth during the pandemic have unsurprisingly proved to be most susceptible to rising interest rates.

Canadian financial services firm Desjardins released what it said was a fairly bearish outlook for house prices back in June, when it suggested house prices would fall 15% on a national basis by the end of 2023. The company now expects the peak to trough fall of somewhere between 20% and 25%, according to updated forecasts published this week.

Similarly, New Zealand's annual rate of house price growth has now fallen into negative territory for the first time in eleven years. The Reserve Bank of New Zealand, which is likely to deliver a fourth consecutive 0.5% rate hike next week, is expecting prices to fall 8.1% this year. Likewise, house prices in Sweden are now declining markedly - the central bank is expecting a peak to trough decline of more than 16% by the end of 2023.

Underscoring what a remarkable period the past two and a half years have been, none of these falls would put average house prices below the level they were at the outset of the pandemic. A reminder that we published our own forecasts for prime house prices in global cities earlier this week.

Peak inflation?

The US consumer price index rose 8.5% during the year to July, down from a 9.1% increase a month earlier, according to the official reading published Wednesday.

The slowing was largely due to falls in the price of gasoline. Core inflation, which strips away energy and food prices, rose 0.3% month-on-month, down from 0.7% in June. That brings the annual rate of growth to 5.9%.

There was a fairly measured relief rally in most global stock markets and it does look likely that inflation is peaking. However, the rate is still well above the Fed's target and much remains uncertain as to how long rising prices will take to unwind.

In other news...

More from our team:

Rising interest rates and debt costs drive repricing in prime logistics markets.

Spanish construction rises despite spiralling costs.

Film & TV Studios - a spotlight on Manchester.

Elsewhere - Luxury watch prices plummet on weak Chinese consumer confidence (FT).