Lettings market in prime London ends year on a positive

December 2021 PCL lettings index: 150.1

December 2021 POL lettings index: 160.1

2 minutes to read

Nine months ago, few would have predicted that rents would end the year in positive territory in the prime London lettings market.

Thanks to a sharp retreat in supply and the physical re-opening of offices and Universities, that is precisely what happened.

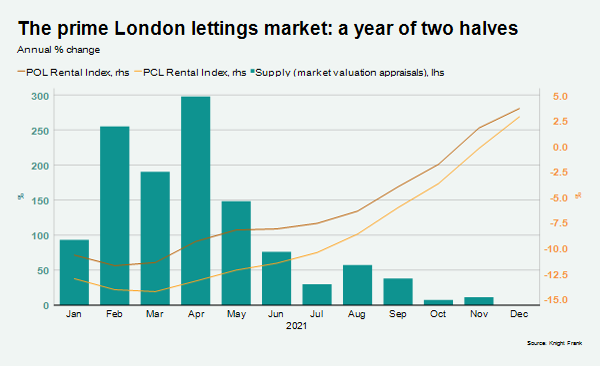

Supply surged dramatically in the early months of this year thanks to the closure of the short-let staycation market, as the chart below demonstrates.

In February, the number of market appraisals, which is when a landlord requests a valuation for the purposes of listing, was 255% higher than the same month in 2020. By November, the increase had narrowed to 11%, with a large number of Airbnb-type properties back on the short-let market.

This precipitous drop in supply drove rents higher, with average rental values climbing 2.9% in the year to December in prime central London (PCL). In prime outer London (POL), there was a 3.7% rise.

These increases at the year-end compare to double-digit declines recorded just nine months ago. Indeed, the six-month increase of 8.2% in PCL in December is the highest recorded over an equivalent period since December 2010. A corresponding rise of 7.1% in POL was last exceeded in September 2007.

We explore some of the dynamics behind the recent growth across individual areas of London in more detail here.

What next?

In addition to falling supply, demand continues to get stronger.

In the three months to November, the number of new prospective tenants increased by 28% compared to the same period in 2020.

Meanwhile, the number of tenancies started was up by 16%.

All things being equal, we would expect these trends to continue in 2022, putting further upwards pressure on rental values and yields.

The emergence of the Omicron variant of Covid-19 means all things may not be equal and its longer-term impact is still uncertain.

However, it would take more than a minor setback to put a meaningful dent in this rental recovery. It would require a rapid rewind to the start of this year, when the vaccination programme was in its infancy, staycations were banned, offices were firmly closed and all University lectures were online.

More will become clear with the pandemic in the coming weeks.