Daily Economics Dashboard - 19 March 2021

An overview of key economic and financial metrics.

2 minutes to read

Download an overview of key economic and financial metrics on 19 March 2021.

Equities: Globally, stocks are mostly lower. In Europe, declines have been recorded by the FTSE 250 (-0.6%), CAC 40 (-0.5%), STOXX 600 (-0.3%) and DAX (-0.2%) this morning. In Asia, the CSI 300 (-2.6%), Hang Seng (-1.4%), KOSPI (-0.9%) and S&P / ASX 200 (-0.6%) all closed lower. The TOPIX was the exception, up +0.2% on close. In the US, futures for the S&P 500 are currently flat, while the Dow Jones Industrial Average is up +0.2%.

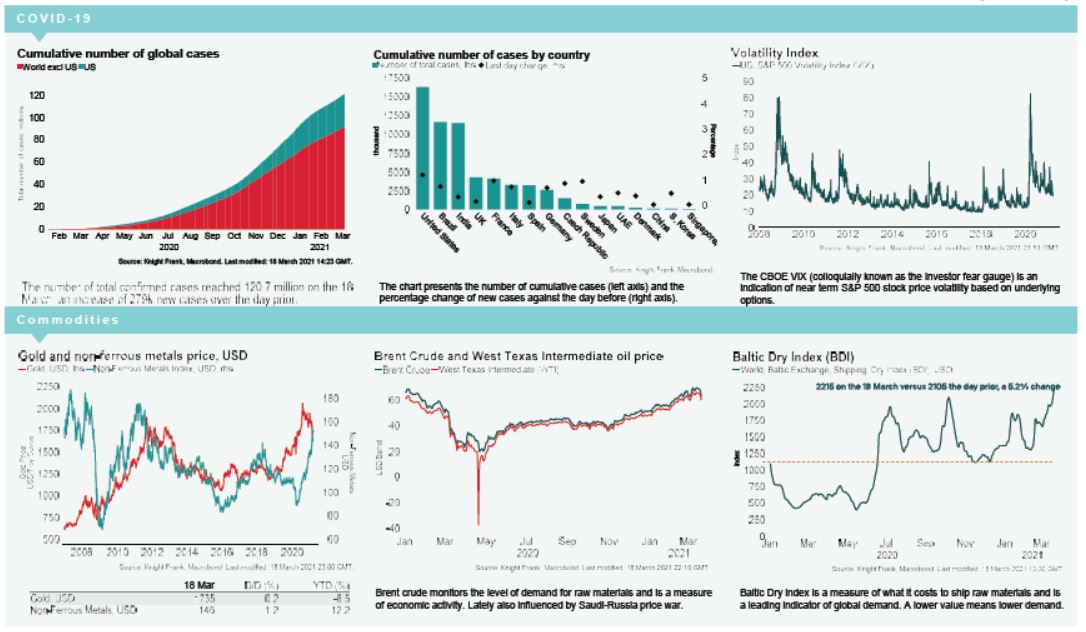

VIX: After increasing +12% over Thursday, the CBOE market volatility index is currently down -2.4% this morning to 21.1, above its long term average (LTA) of 19.9. The Euro Stoxx 50 volatility index is also higher, up +6.0% to 18.5, albeit, remaining below its LTA of 23.9.

Bonds: The UK 10-year gilt yield has compressed -5bps to 0.83%, the German 10-year bund yield is down -3bps to -0.31% and the US 10-year treasury yield is -1bp lower at 1.69%.

Currency: Sterling has depreciated to $1.39, while the euro is currently $1.19. Hedging benefits into the UK and the Eurozone are 0.53% and 1.68% on a five-year basis.

Oil: Both Brent Crude and the West Texas Intermediate (WTI) declined -7% over Thursday, however, this morning they have since increased +1.1% and +1.3% to $63.95 and $60.76 per barrel, respectively.

Baltic Dry: The Baltic Dry increased for the fourth consecutive session on Thursday, up +5.2% to 2215, its largest daily increase in over a month and its highest level in 18 months. Panamax rates have pushed prices higher, up +9.3% yesterday to their highest level since September 2010. Capesize rates were also higher, up +5.3%, their strongest level since 26th January 2021.

US Unemployment: There were 770k new unemployment applications in the week to 13th March, above market expectations of 700k and higher than 725k last week. This is the highest reading in a month.

UK Debt: Public sector net borrowing (excluding public sector banks) totalled £19.1bn in February, £17.6bn higher than a year prior and the highest February figure since ONS records began. With one month of the fiscal year left, 2020 – 2021 borrowing is currently £278.8bn, below the £355bn forecast by the OBR for the full fiscal year.