Record activity in prime London will come under pressure after the summer

June 2022 PCL sales index: 5457.6

June 2022 POL sales index: 274.8

3 minutes to read

Last quarter was an undeniably strong period for the prime London property market - the question is how long it will last.

Supply continued to catch up with demand, which was the key reason for such high trading volumes.

The number of new sales instructions (supply) in Q2 was the third highest figure in a decade while the number of new prospective buyers (demand) was the second highest total over the last ten years, Knight Frank data shows.

The result was the highest number of offers accepted since 2012 and the third highest number of exchanges.

Demand far exceeded supply during the frenetic trading conditions of the 14-month stamp duty holiday, which ended last September. Property sold so quickly that prospective sellers held back due to a lack of purchase options, creating a vicious circle effect.

That only slowly reversed, and activity levels have built to a crescendo in the late spring/early summer, supported by the fact London has regained its gravitational pull as offices re-opened and normal city life resumed.

So, how sustainable is the current period of strong trading?

Rising mortgage rates will eventually begin to curb demand, which will happen to a greater extent in lower price brackets and domestic-driven markets.

Higher levels of affluence, housing equity and a broader base of international buyers will support demand in prime central London (PCL) even as the cost-of-living squeeze gets tighter.

For now, the prospect of higher borrowing costs is bringing buyers and sellers forward.

“The combination of pent-up demand from the era of low-supply and a desire to act before mortgage rates rise further explains why trading is so robust at the moment,” said Tom Bill, head of UK residential research at Knight Frank. “The market is in the sort of sweet spot that doesn’t last forever.”

Another drag on activity, particularly over the summer, will be the return of seasonality as more buyers and sellers take a holiday. Staff shortages within the conveyancing chain are also prolonging transaction times.

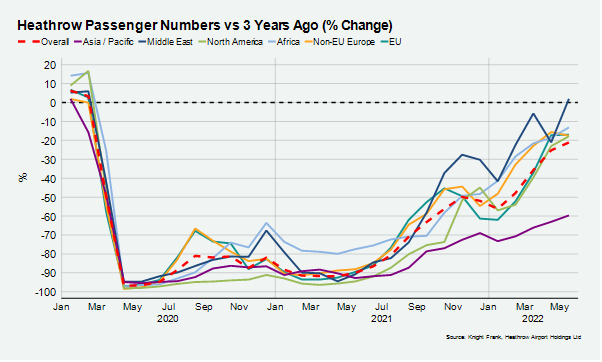

Meanwhile, international travel restrictions will keep a lid on demand and prices in prime central London while they remain in place.

There is still a wide divergence in terms of international passenger numbers compared to 2019. The overall figure was 21% lower in May, but it was greater for Asia Pacific (-60%), where many countries still have tighter Covid restrictions. While the number was higher for the Middle East in May 2022 compared to 2019, this was due to the timing of Ramadan.

Average prices in PCL increased 2.5% in the year to June as they continued their gradual recovery after seven years of political uncertainty and tax hikes. It was a modest rise but the strongest rate of growth since April 2015.

Furthermore, strong domestic demand, a weak pound and the appeal of property compared to other asset classes means sales above £10 million are at a six-year high, as we explore here in more detail.

In prime outer London, annual growth reached 5.1% after quarterly growth slowed for the fourth month in a row, underlining how the race for space is calming down.

In summary, we expect the current strong period of trading to come under pressure after the summer. In PCL, the effect will be less marked depending on how quickly international travel resumes.

For more detail on what we believe will happen this year and next, please see our latest price forecasts here.