Art leads 2023 Luxury Investment Index

Art once again tops the Knight Frank Luxury Investment Index (KFLII) in Q2, as growth starts to slow or reverse for some other asset classes tracked by the index.

6 minutes to read

Last updated: 08/08/2023

The update for Q2 comes from the Luxury Investments report from The Wealth Report Series, giving high-net-worth-individuals a guide to investments of passion.

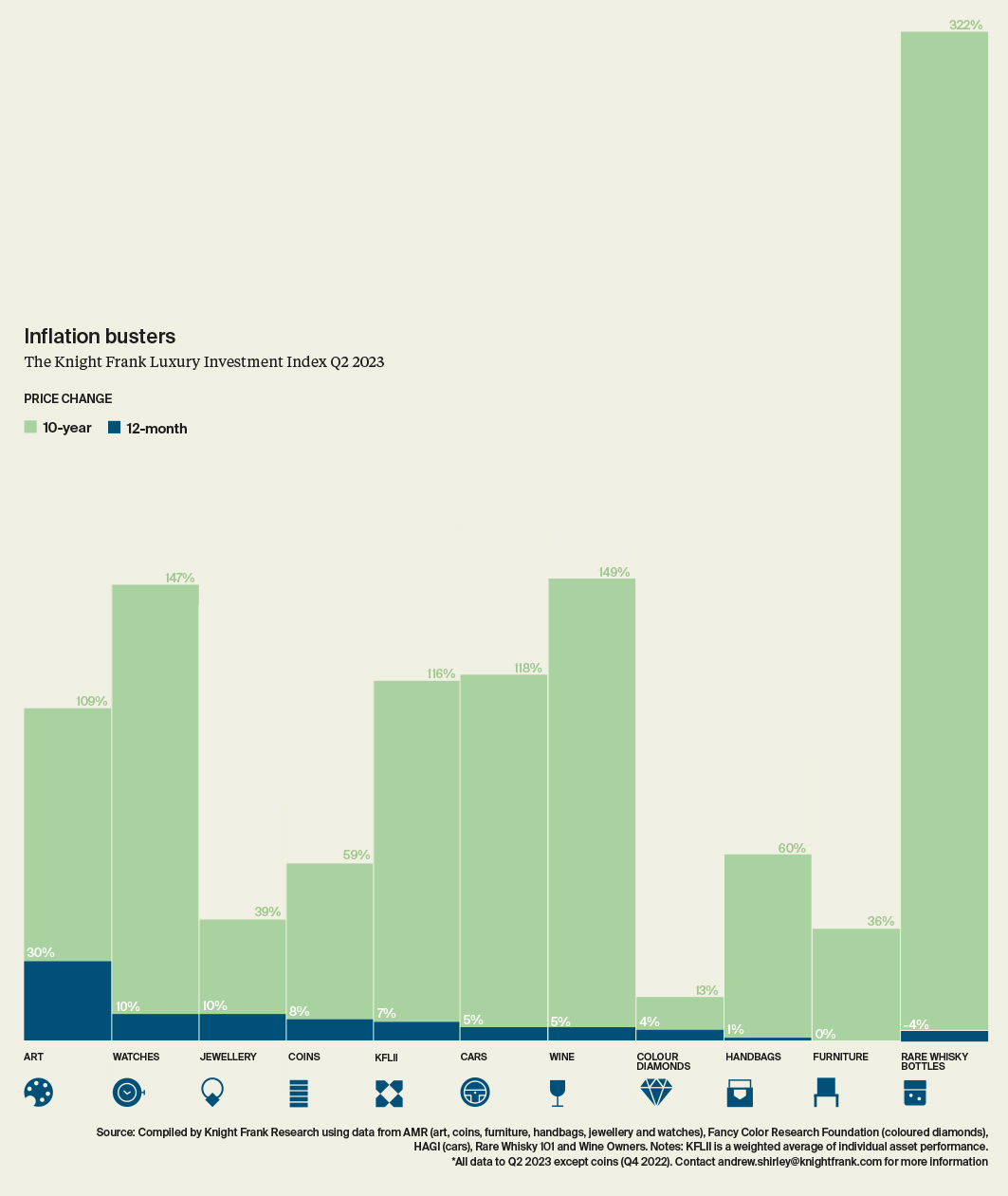

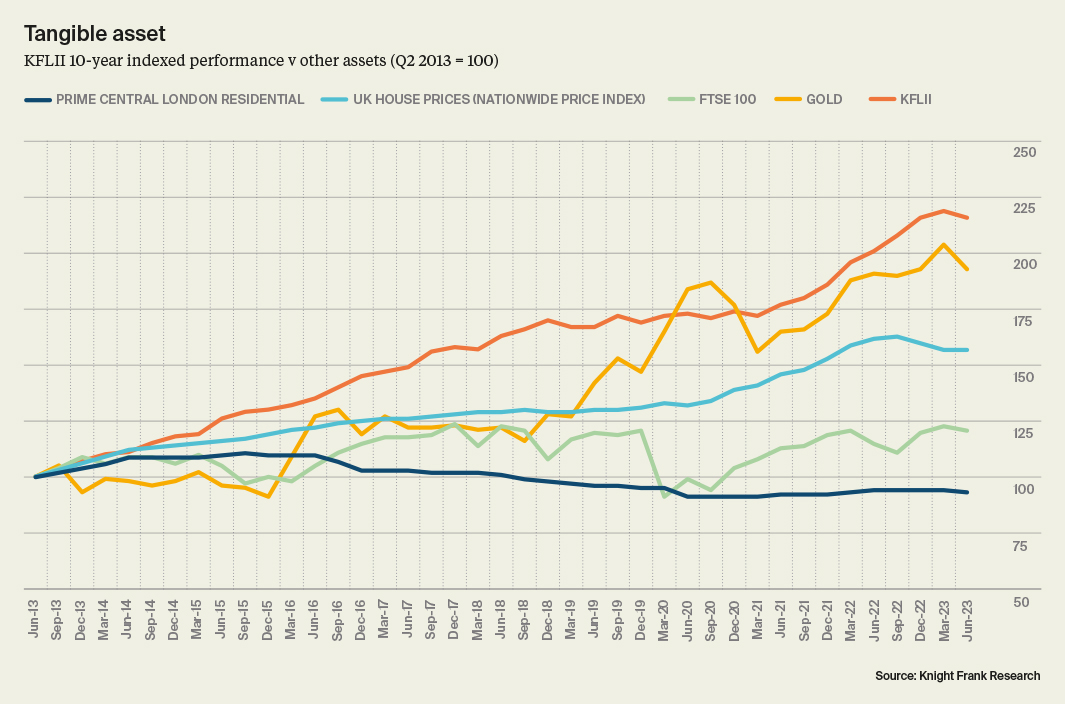

The Knight Frank Luxury Investment Index (KFLII), which tracks a weighted basket of 10 collectibles, rose by 7% in the 12 months to the end of June 2023.

This was a creditable performance compared with houses in Prime Central London, down 1% over the same period; the FTSE 100 index of equities, which rose by 5%; and gold which was up in value by just 1%. But it was the weakest annual performance by KFLII since Q2 2021, proving that even tangible assets are not immune to market uncertainty.

A slowdown in the wine and classic car markets, where double-digit rises have often underpinned the index’s performance, helped temper growth.

Art

Even the performance of art, which tops KFLII with 12-month growth of 30%, as measured by AMR’s All Art index, should be understood in terms of the post pandemic recovery period rather than just a market in robust health, reckons AMR’s Sebastian Duthy.

“The auction season’s spring sales are the first measure of market confidence and recent results suggest growth is already starting to slow. While it’s tempting to connect the fortunes of the art market with current external events, big changes to the way auctioneers do business is equally important to factor in,” notes Sebastian.

“The days when the top auction houses relied on the three Ds – Death, Debt and Divorce – are long gone. Go to Sotheby’s website and you will find auctions appear secondary to the number of pages offering private sales on anything from sneakers and barware to pens and lighters. Today, headline-grabbing public sales of art act more as a marketing tool attracting collectors to the increasingly popular luxury sector.

“And while it remains true that the best works by Picasso, Warhol and others continue to achieve walletbusting- prices, less iconic pieces by these artists often struggle to reach estimates. AMR’s All Art ‘Top Traded’ index tracks the most liquid sector of the market by analysing only artists who have had 30 or more sales in a twoyear period. This index is dominated by artworks from impressionist, modern and contemporary masters and reveals how average values have moved little since 2016,” he says.

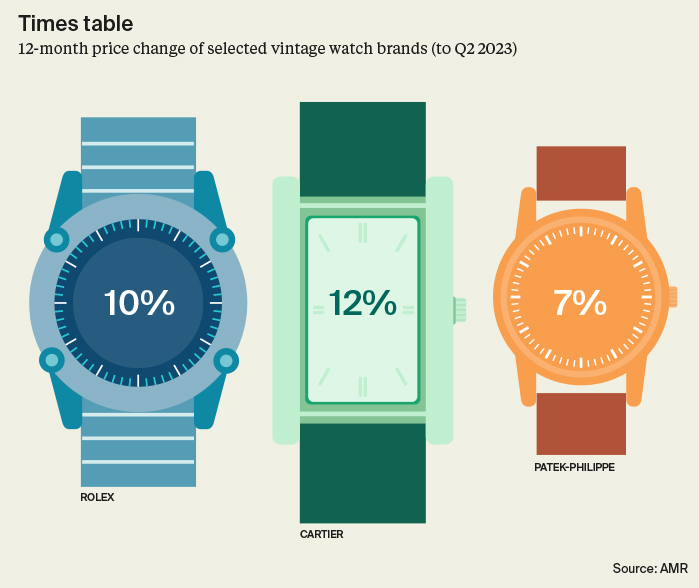

Watches

Wearable investments of passion like jewellery and watches, seem to have retained their allure, for now at least. The AMR Watch index was up 10%, but “a correction may be on the cards for some hyped watch styles,” says Sebastian.

“But collectors from around the world were drawn to vintage jewels and exceptional coloured gemstones and diamonds as they re-invigorated recent summer auction sales,” he points out. “Christie’s had an exceptional season of jewellery sales in the first half of 2023, including the record-breaking single-owner sale of the Collection of Heidi Horten. A ruby and diamond ‘bird of paradise’ brooch by Van Cleef & Arpels sold for 453,000 Swiss francs in Geneva in May 2023, up by around 40% compared with a sale of the same piece in 2018.”

Classic cars

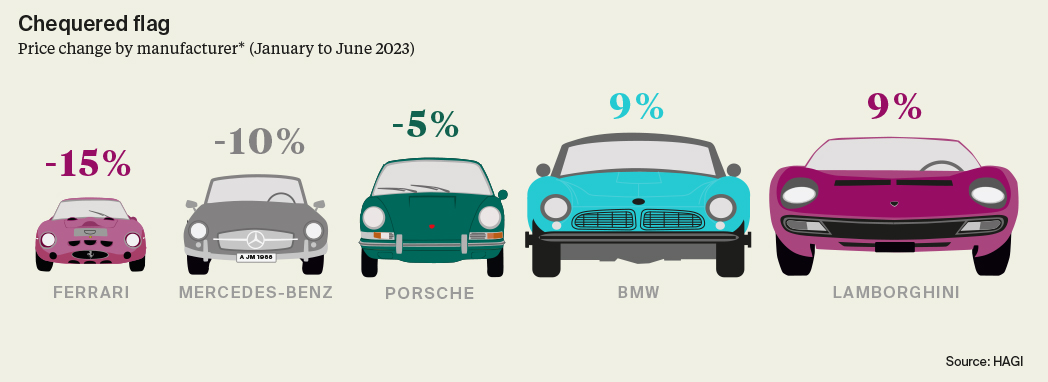

The performance of classic cars has been mixed, says Dietrich Hatlapa of our data provider HAGI.

“After a strong performance in 2022 when the value of the most investable classic cars rose by 25%, this year has seen the market slip into reverse gear due to macroeconomic factors like rising interest rates and inflation.”

According to the HAGI Top Index, prices dropped by almost 7% in the first half of the year. Ferrari experienced the most significant decline, falling slightly more than 15%.

Nonetheless, not every vehicle is veering off the course. The Lamborghini Index of HAGI has increased by 9% this year to date, similar to its newly introduced BMW index.

“These cars tend to be a bit newer and offer low price points for collectors,” says Dietrich. “Very strong communities of collectors have also built up around iconic models like the Miura,” he adds.

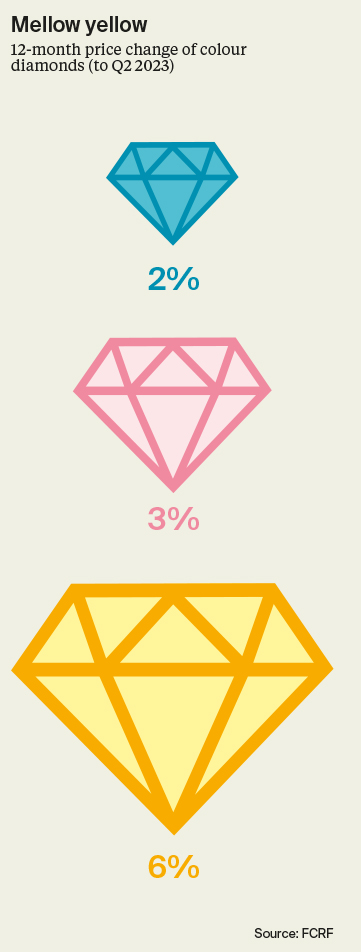

Colour Diamonds

Colour diamonds are enjoying a rise in interest, says Miri Chen of the Fancy Colour Research Foundation.

“As for the shift from colourless to fancy colour, we see more wholesalers who are looking for safer areas to invest their capital. As a result, many of them increase their fancy colour diamonds at the expense of their colourless inventory.

“We do observe a dramatic change in the way retailers present fancy colour diamonds,” adds Miri. “The feedback we receive indicates a significant increase in the success rate of fancy colour sales when even inexperienced sales teams use our research to engage in fascinating conversations with collectors to convey genuine appreciation and an emotional connection.”

Although pink diamonds have seen the strongest price growth over the long term, yellow diamonds have been rising in popularity over the past 12 months, according to the latest FCRF data.

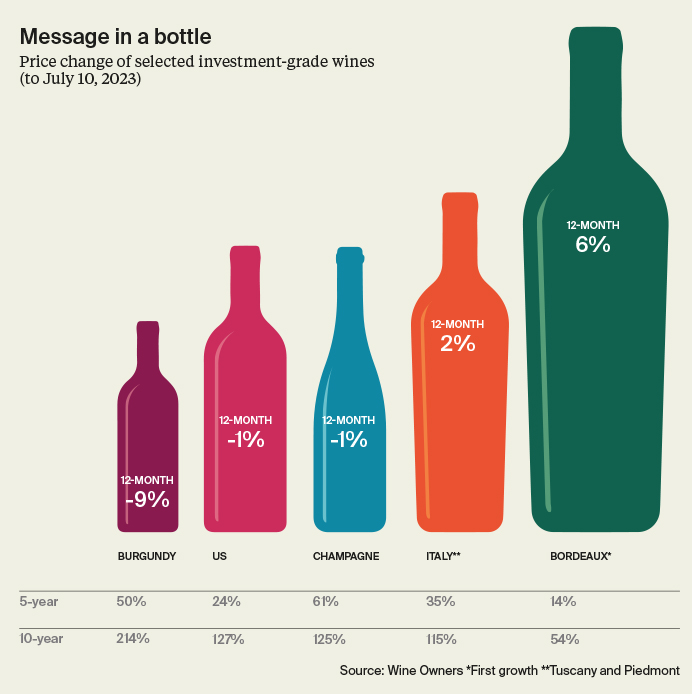

Wine and Whisky

“Burgundy has been the big success story of the past decade, with prices having escalated 367% by the early autumn of 2022. However, the top of the Burgundy market peaked around that time and has since fallen by at least 9%. Published prices tend to lag realised sales, indicating that there is further to fall,” points out Nick Martin of Wine Owners, which compiles the Knight Frank Fine Wine Icons Index (KFFWII).

“Whereas Burgundy is scarcity led, Champagne is a high-volume market, with certain prestige brands’ production running into the several million of bottles per vintage release. Prices of some of those prestige cuvées have been testing price elasticity of demand and seen sales stagnate as a result,” adds Nick.

“Against this backdrop the KFFWII, benefitting from its globally balanced index composition, has risen 5% in the past year and is flat year to date.

Nevertheless, the heightened cost of capital may well act as drag on blue chip fine wine markets for the rest of 2023,” Nick predicts.

“When interest rates have risen sharply to around 6%, new releases in particular, according to market economics, should be offered at a bigger discount to future value in order to convince consumers to spend on wine instead of holding cash. If wine markets are looking toppy with limited obvious upside for new releases, there’ll continue to be downward pressure exerted on secondary market prices more widely,” he explains.

Some markets like South Africa (+11%) and Australia (+8%) have, however, seen strong growth this year.

However, rare bottles of whisky, our strongest 10-year performer by far, are the only KFLII asset class to actually see a negative annual performance dropping by 4%, according to the index compiled for us by Rare Whisky 101.

“Bottles of rare whisky have had a far more sedate time from a performance perspective over the past three years,” confirms Andy Simpson of industry consultant Simpson Reserved. “Higher value (over £5,000) bottles have re-traced recently due to a myriad of geo-political, social and economic reasons.

Certain brands have still performed well, while the market leader (from a sheer volume of market perspective), Macallan, has seen particularly punishing losses with its index re-tracing almost 12% over the past twelve months,” says Andy.

Discover more

Download

Download the full report for a unique guide to the investments of passion collected by high-net-worth-individuals.

Download the report

Subscribe

Subscribe for all the latest insights and additional content from The Wealth Report.

Subscribe