Strong pricing for industrial assets driving sustained rise in sale and leasebacks

Balance sheet management and strong pricing for industrial assets drives upsurge in corporate asset sales.

4 minutes to read

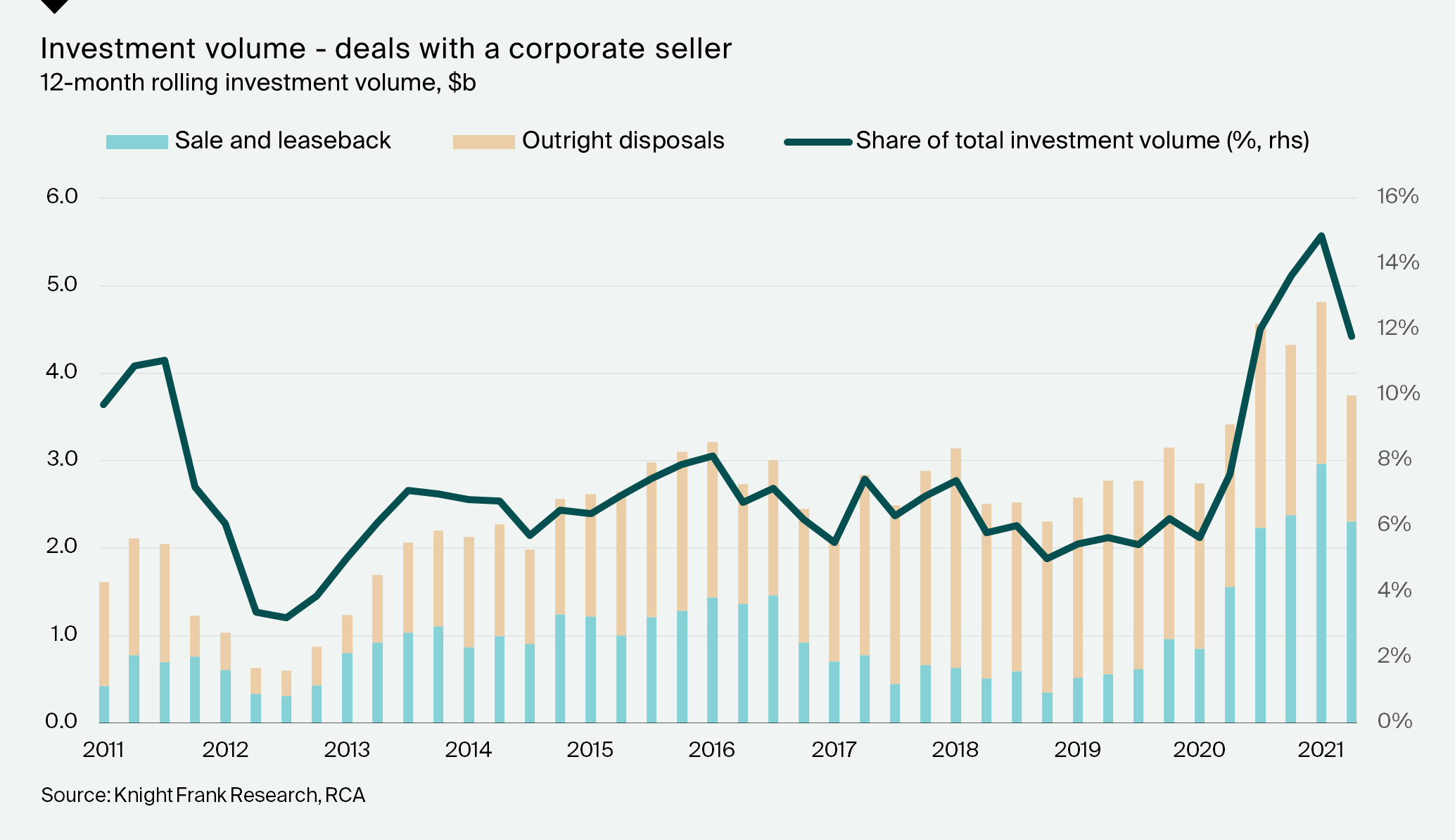

Over the past year, deals involving a corporate seller as a share of total commercial investment volume have increased significantly. The increase has predominately been driven by sale and leaseback deals as corporates look to repair their balance sheets in the wake of the pandemic downturn, and take advantage of historically low yields.

Deals involving a corporate seller have increased notably since the onset of the pandemic. Over the year to June 2021, there have been $3.7 billion of assets sales accounting for 11.8% of total investment volume, compared to 7.6% a year earlier and 5.7% over the 12 months to March 2020.

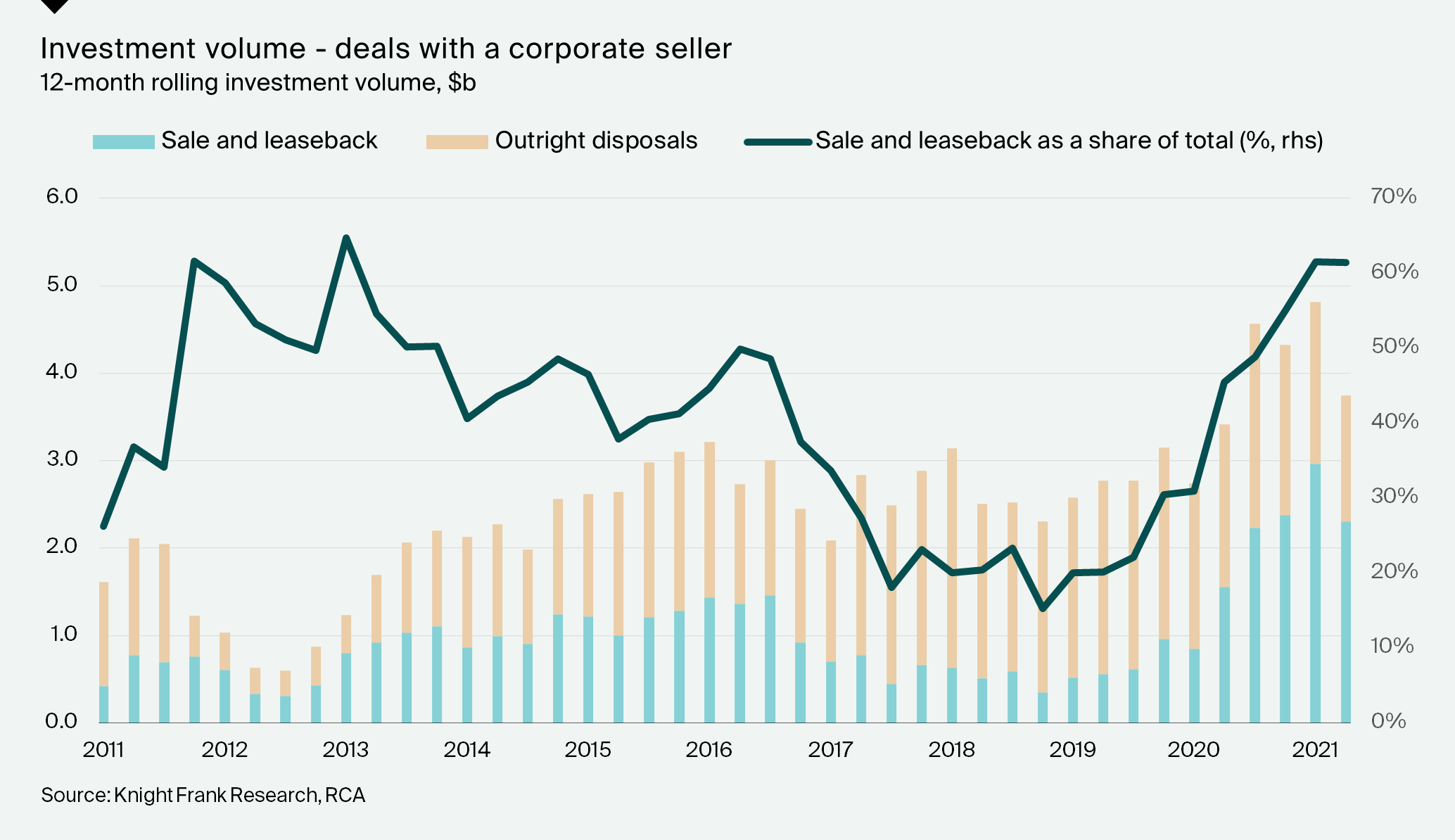

The increase in deals involving a corporate seller has been largely driven by sale and leaseback deals rather than outright disposals. Sale and leaseback deals accounted for 61% of deals with a corporate seller over the year to June 2021, up from 46% a year earlier, and the highest level since Q1 2013.

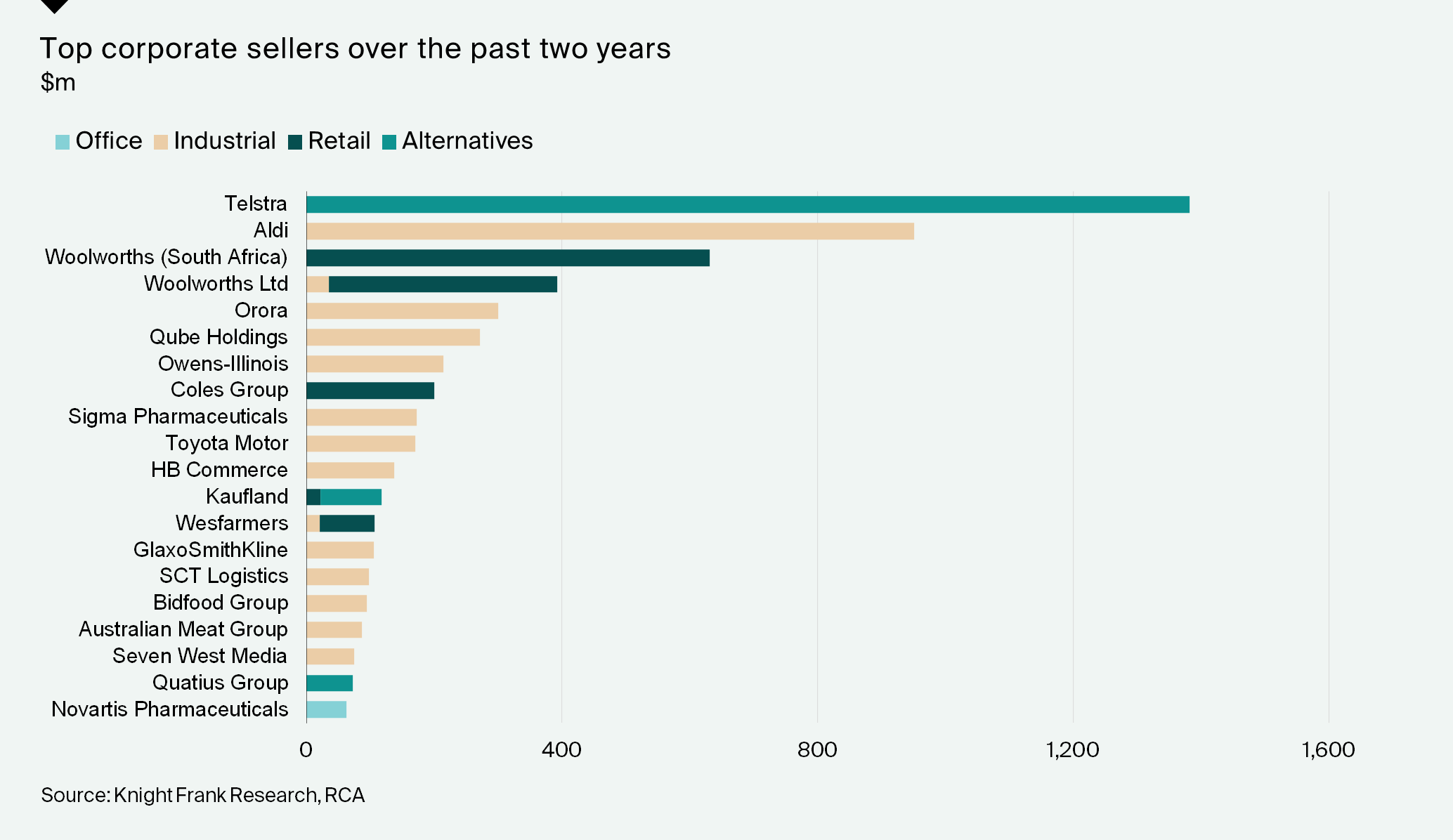

By sector, industrial, retail, and alternatives (data centres) assets have accounted for a large share of deals involving a corporate seller, underpinned by a number of large deals including:

- Telstra’s sale and leaseback of its data centre in Clayton in Melbourne to Centuria Industrial REIT for $416.7 million in August 2020, and the disposal of the Pitt Street Exchange in Sydney to Charter Hall Long WALE REIT for $281.5 million.

- Aldi’s disposal of four distribution centres to Charter Hall and Allianz Real Estate for $648 million in June 2020, and a further two distribution centres to the same buyers for $281.5 million in December 2020.

- The sale of the David Jones store on Elizabeth Street in the Sydney CBD by Woolworths (South Africa) to Charter Hall for $510 million in December 2020.

Qube Holdings’ pending disposal of the Moorebank Logisitics Park in Sydney to Logos for $1.65 billion will further boost investment volume upon settlement.

Rise in corporate sales driven by balance sheet management and low yields

There are two principal drivers for the rise in companies selling property holdings (especially through sale and leaseback deals) over the past year.

Firstly, it reflects the desire to support corporate balance sheets and rebalance asset holdings amidst the pandemic.

For some companies, trading conditions over the past year have presented a serious challenge to cash flow and this has motivated the desire to shore up balance sheets via asset sales.

For other companies, there was no material threat to cash flow but asset sales have been pursued to free up capital to deploy opportunistically as they reassess their business models and reconfigure their operations in the wake of pandemic-related disruption.

Secondly, companies have also sought to take advantage of historically low yields on many commercial property assets which have resulted in rising values and hence the scope to realise substantial capital gains on long-standing property holdings.

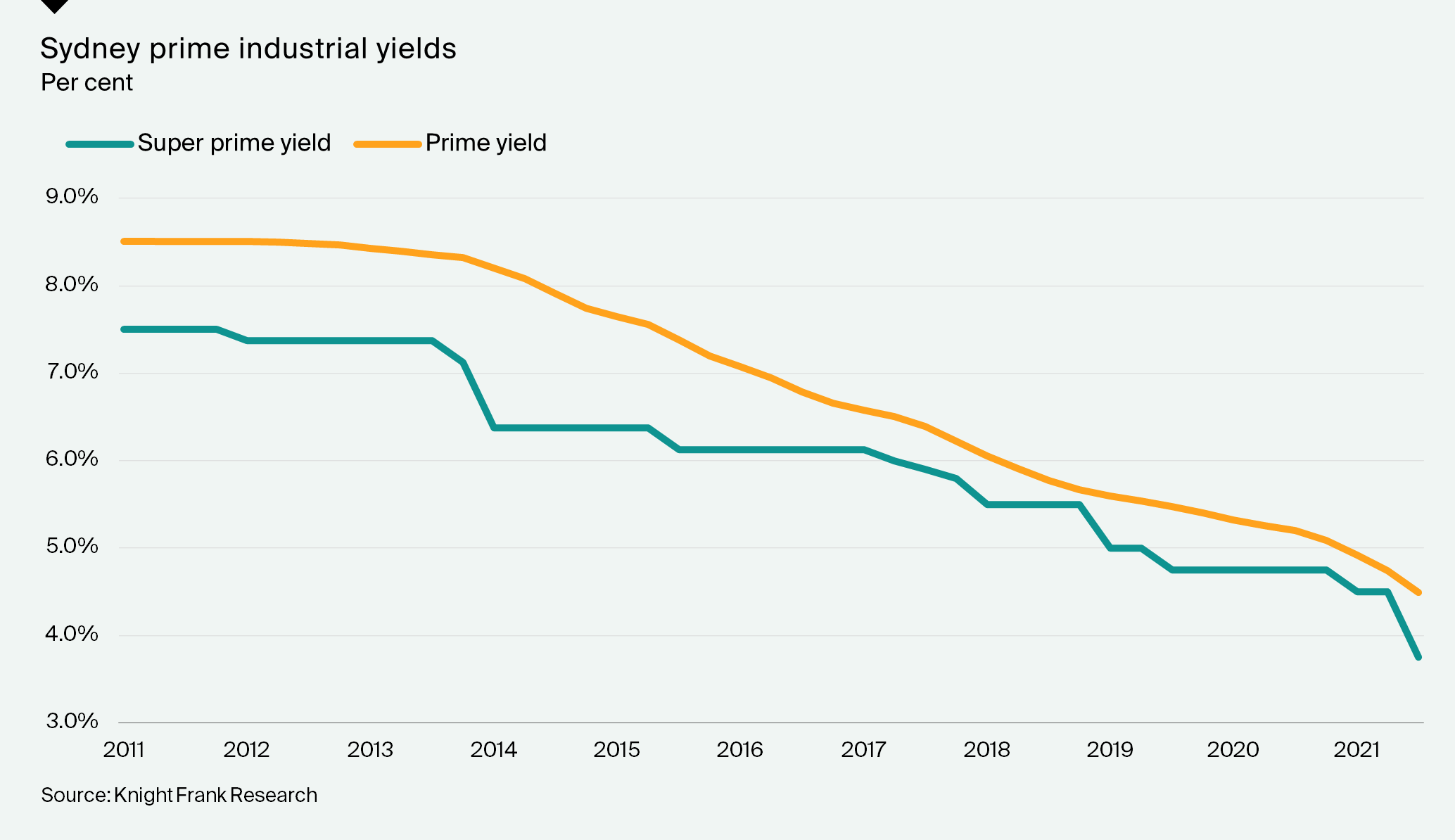

With the notable exception of the retail sector, property yields have generally continued to drift lower over the past few years consistent with the shift downward in interest rates since mid-2019. Yield compression has been particularly pronounced in the industrial sector, with demand for logistics assets boosted by the acceleration of growth in e-commerce and the trend towards online shopping. The growth of the sector has spurred the development of larger and more sophisticated buildings with long leased income streams and yields for these types of assets are now now moving below 4.0% in Sydney and Melbourne.

Companies have taken advantage of this environment to sell (and often leaseback) assets, with the industrial and logistics sector accounting for 48% of deals with a corporate seller over the year to June 2021.

Looking ahead, the economic recovery should continue to ease the pressure on corporate balance sheets, barring any significant ill effects from renewed lockdowns in Sydney and Melbourne. At one level this will reduce the impetus for companies to monetise their property assets. Indeed, the share of deals with a corporate seller has moderated a little from its recent peak of 14.9% of total investment volume recorded over the year to March 2021, although it remains high by historical standards.

However, the prolonged low interest rate environment in Australia and globally, and the likelihood that this will continue indefinitely, will ensure yields remain low. Related to this, intense competition for property assets, including from major global investors with a significantly lower cost of capital and commensurately lower target returns than most corporate property owners, will continue to drive strong pricing, particularly for industrial and logistics assets and alternative assets such as data centres, and this will continue to motivate corporate property holders to take advantage through asset sales.

For further information please contact:

Chris Naughtin

Director, Research & Consulting

+61 2 9036 6794

Chris.Naughtin@au.knightfrank.com

Ben Burston

Partner, Chief Economist

+61 2 9036 6756

Ben.Burston@au.knightfrank.com